How to Buy Your First Home in the Philippines (2026 Guide)

Paano Bumili ng Unang Bahay Mo sa Pilipinas (2026 Gabay)

5 Things to Know

First home in five facts.

Quick Summary

Mabilis na Buod

Important Disclaimer

This guide is for educational purposes only and does not constitute financial, legal, or real estate advice. GabayPH is not a licensed real estate broker, financial advisor, or lawyer. Property laws, loan terms, and processes may vary by location and may change without notice. Consult a licensed real estate broker, lawyer, and/or financial advisor before making any property purchase decisions. GabayPH has no paid relationship with any bank, developer, or real estate company mentioned in this guide.

Mahalagang Disclaimer

Ang gabay na ito ay para sa layuning pang-edukasyon lamang at hindi bumubuo ng financial, legal, o real estate advice. Ang GabayPH ay hindi isang lisensyadong real estate broker, financial advisor, o abogado. Ang mga batas sa property, loan terms, at proseso ay maaaring mag-iba sa bawat lokasyon at maaaring magbago nang walang paunang abiso. Kumonsulta sa isang lisensyadong real estate broker, abogado, at/o financial advisor bago gumawa ng anumang desisyon sa pagbili ng property. Walang bayad na relasyon ang GabayPH sa kahit anong bangko, developer, o real estate company na binanggit sa gabay na ito.

Table of Contents

- Home Buying Overview

- Buying from a Developer vs Private Seller

- Understanding Titles: TCT vs CCT

- What "Clean Title" Means

- Requirements and Documents

- Step-by-Step Process

- Pag-IBIG Housing Loan

- Bank Housing Loans Compared

- How to Check for Liens at Registry of Deeds

- Transfer of Title Process

- Real Property Tax Basics

- Common Scams to Avoid

- Pro Tips

- Frequently Asked Questions

Talaan ng Nilalaman

- Pangkalahatang-tanaw sa Pagbili ng Bahay

- Pagbili mula sa Developer vs Private Seller

- Pag-unawa sa Titulo: TCT vs CCT

- Ano ang Ibig Sabihin ng "Clean Title"

- Mga Requirements at Dokumento

- Hakbang-Hakbang na Proseso

- Pag-IBIG Housing Loan

- Mga Bank Housing Loan na Pinaghahambing

- Paano Mag-check ng Liens sa Registry of Deeds

- Proseso ng Transfer ng Titulo

- Basics ng Real Property Tax

- Mga Karaniwang Scam na Dapat Iwasan

- Mga Payo

- Mga Madalas Itanong

Home Buying Overview

Pangkalahatang-tanaw sa Pagbili ng Bahay

Buying your first home is one of the biggest financial decisions you'll ever make. In the Philippines, the median price for a house and lot in Metro Manila ranges from ₱2-5 million for socialized/economic housing, ₱5-15 million for mid-range, and ₱15 million+ for high-end properties. Outside Metro Manila, prices can be 30-60% lower.

Ang pagbili ng unang bahay mo ay isa sa pinakamalaking financial decisions na gagawin mo. Sa Pilipinas, ang median price para sa house and lot sa Metro Manila ay nasa ₱2-5 milyon para sa socialized/economic housing, ₱5-15 milyon para sa mid-range, at ₱15 milyon+ para sa high-end properties. Sa labas ng Metro Manila, ang mga presyo ay maaaring 30-60% mas mababa.

There are three main ways to finance your purchase:

May tatlong pangunahing paraan para pondohan ang pagbili mo:

- Pag-IBIG Housing Loan — The most affordable option with the lowest interest rates (5.375-10.375% per year). Maximum loanable amount: ₱6 million. Requires 24 months of Pag-IBIG contributions. Best for: salaried employees and OFWs. See our full Pag-IBIG guide.

- Bank Housing Loan — Higher loan amounts (up to ₱20-50 million+), faster processing, but higher interest rates (6-10%+ per year). Best for: professionals with higher income who need larger loans or faster approval.

- In-house financing (Developer) — Financing directly from the property developer. Easiest to qualify for, but has the highest interest rates (12-18%+ per year) and shortest terms (5-15 years). Best for: those who can't qualify for bank or Pag-IBIG loans, or as short-term bridge financing.

- Pag-IBIG Housing Loan — Ang pinaka-affordable na opsyon na may pinakamababang interest rates (5.375-10.375% kada taon). Maximum loanable amount: ₱6 milyon. Kailangan ng 24 buwan na Pag-IBIG contributions. Pinakamahusay para sa: salaried employees at OFWs. Tingnan ang buong Pag-IBIG guide namin.

- Bank Housing Loan — Mas mataas na loan amounts (hanggang ₱20-50 milyon+), mas mabilis na processing, pero mas mataas na interest rates (6-10%+ kada taon). Pinakamahusay para sa: mga propesyonal na may mas mataas na income na kailangan ng mas malalaking loans o mas mabilis na approval.

- In-house financing (Developer) — Financing direkta mula sa property developer. Pinakamadaling ma-qualify, pero may pinakamataas na interest rates (12-18%+ kada taon) at pinakamaikling terms (5-15 taon). Pinakamahusay para sa: mga hindi makapag-qualify sa bank o Pag-IBIG loans, o bilang short-term bridge financing.

Buying from a Developer vs Private Seller

Pagbili mula sa Developer vs Private Seller

Buying from a Developer

The most straightforward option for first-timers. Developer handles most paperwork and offers structured payment terms.

- Watch out for: Premium pricing, possible construction delays, steep pre-selling amortization, monthly condo dues.

- Key check: Verify the developer has a License to Sell from DHSUD. Never buy without this.

Buying from a Private Seller

Often 10-30% cheaper than developer prices, but requires more due diligence.

- Watch out for: Title issues, hidden defects, complex paperwork — you handle everything yourself.

- Key check: Verify the title at the Registry of Deeds, check for liens, and hire a lawyer to review the Deed of Sale before signing.

Pagbili mula sa Developer

Pinaka-straightforward na opsyon para sa mga first-timers. Hinahawakan ng developer ang karamihan ng paperwork at nag-o-offer ng structured payment terms.

- Bantayan: Premium pricing, posibleng construction delays, mataas na pre-selling amortization, buwanang condo dues.

- Key check: I-verify na may License to Sell mula sa DHSUD ang developer. Huwag bumili nang wala ito.

Pagbili mula sa Private Seller

Kadalasang 10-30% na mas mura kaysa sa developer prices, pero mas maraming due diligence ang kailangan.

- Bantayan: Title issues, hidden defects, kumplikadong paperwork — ikaw ang haharap sa lahat.

- Key check: I-verify ang titulo sa Registry of Deeds, mag-check ng liens, at kumuha ng abogado para i-review ang Deed of Sale bago pumirma.

Understanding Titles: TCT vs CCT

Pag-unawa sa Titulo: TCT vs CCT

Two main title types in the Philippines:

- TCT (Transfer Certificate of Title) — for land and house-and-lot. Proves you own the land and structures on it. Registered at the Registry of Deeds.

- CCT (Condominium Certificate of Title) — for condo units. You own the unit + proportionate share of common areas, but NOT the land (owned collectively via the condo corporation under RA 4726).

Important: Never accept a "tax declaration" as proof of ownership — it only proves someone pays taxes on the property, not legal ownership. Always insist on the original TCT or CCT.

Dalawang pangunahing uri ng titulo sa Pilipinas:

- TCT (Transfer Certificate of Title) — para sa lupa at house-and-lot. Pinapatunayan na ikaw ang may-ari ng lupa at mga istruktura dito. Nakarehistrong sa Registry of Deeds.

- CCT (Condominium Certificate of Title) — para sa condo units. Pag-aari mo ang unit + proportionate share ng common areas, pero HINDI ang lupa (pag-aari ito ng lahat ng unit owners sa pamamagitan ng condo corporation sa ilalim ng RA 4726).

Mahalaga: Huwag tanggapin ang "tax declaration" bilang patunay ng pagmamay-ari — nagpapatunay lang ito na may nagbabayad ng buwis, hindi legal na pagmamay-ari. Palaging humingi ng orihinal na TCT o CCT.

What "Clean Title" Means

Ano ang Ibig Sabihin ng "Clean Title"

A "clean title" means the property title is free from any of the following:

- Liens — Legal claims on the property, such as an existing mortgage, unpaid contractor's work, or court judgments

- Encumbrances — Restrictions on the use or transfer of the property (e.g., easements, right of way, adverse claims)

- Lis pendens — A notice that a lawsuit is pending involving the property

- Annotations — Notes on the title recording mortgages, leases, or other claims

- Dual/overlapping titles — Rare but dangerous cases where two titles exist for the same land

When a seller says the property has a "clean title," you should never take their word for it. Always verify by getting a Certified True Copy of the title from the Registry of Deeds and having it checked by a lawyer.

Ang "clean title" ay nangangahulugang ang titulo ng property ay malaya mula sa alinman sa mga sumusunod:

- Liens — Legal claims sa property, tulad ng existing mortgage, hindi nabayarang trabaho ng kontratista, o court judgments

- Encumbrances — Mga paghihigpit sa paggamit o paglipat ng property (hal., easements, right of way, adverse claims)

- Lis pendens — Paunawa na may pending na kaso na kinasasangkutan ng property

- Annotations — Mga tala sa titulo na nagre-record ng mortgages, leases, o iba pang claims

- Dual/overlapping titles — Bihira pero mapanganib na mga kaso kung saan dalawang titulo ang umiiral para sa parehong lupa

Kapag sinabi ng seller na may "clean title" ang property, huwag kailanman paniwalaang basta-basta. Palaging i-verify sa pamamagitan ng pagkuha ng Certified True Copy ng titulo mula sa Registry of Deeds at ipasuri ito sa abogado.

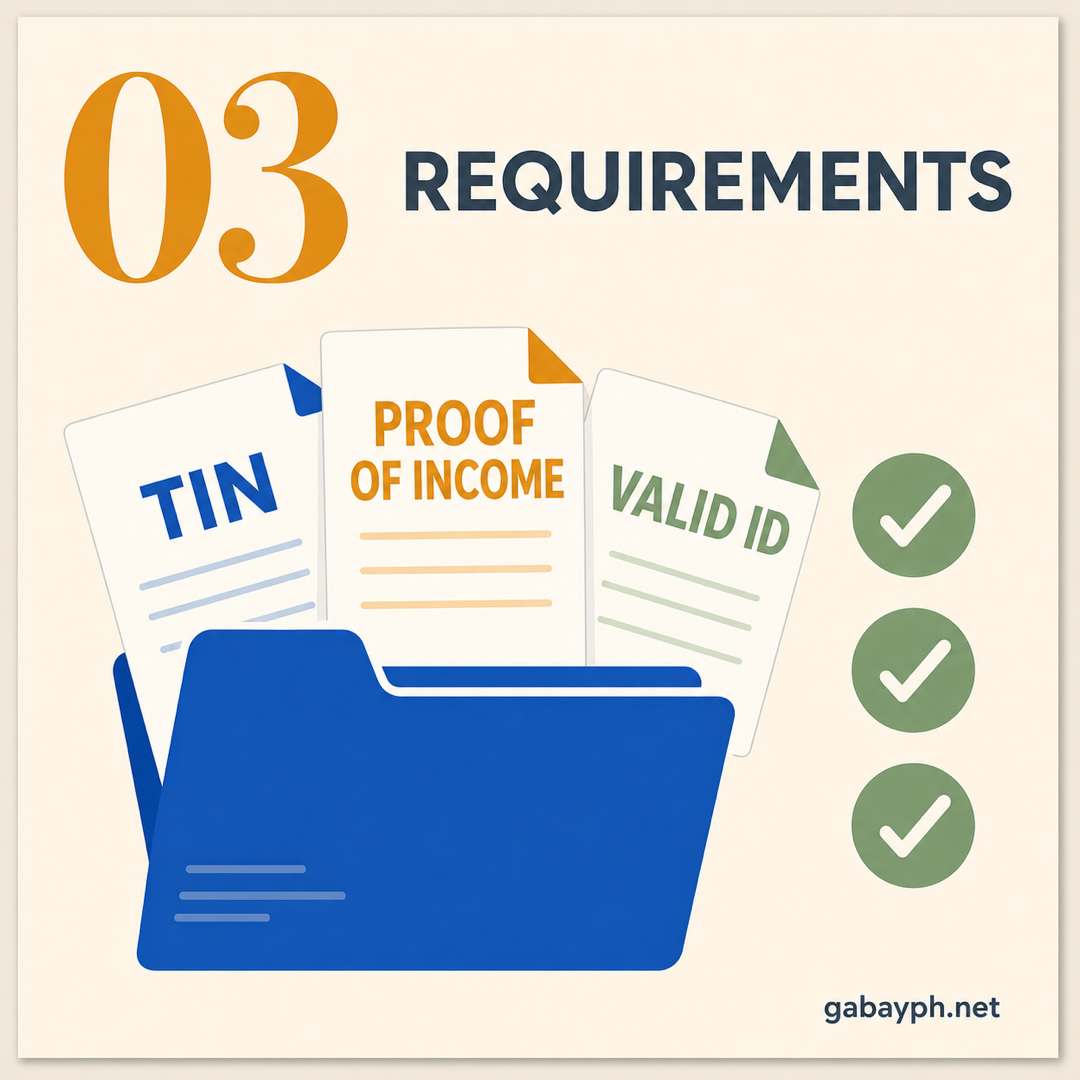

Requirements and Documents

- Valid government IDs (2 copies) — Passport, driver's license, PhilSys ID, UMID, or PRC ID for both buyer and seller

- TIN (Tax Identification Number) — Required for tax payments during transfer. See our TIN guide.

- Proof of income — Latest 3-month payslips, ITR, or Certificate of Employment with compensation (for loan applications)

- Pag-IBIG MID Number + 24 monthly contributions — Required for Pag-IBIG housing loans. See our Pag-IBIG guide.

- Marriage certificate (if married) — Spouse's consent is required for property purchases under the Family Code

- Certified True Copy of the title (TCT/CCT) — Obtained from the Registry of Deeds to verify ownership

- Updated real property tax receipts — Proof that the seller has paid all property taxes up to date

- Tax clearance from the Treasurer's Office — Confirms no outstanding property tax liabilities

Mga Requirements at Dokumento

- Valid na government IDs (2 kopya) — Passport, driver's license, PhilSys ID, UMID, o PRC ID para sa buyer at seller

- TIN (Tax Identification Number) — Kailangan para sa mga tax payments sa panahon ng transfer. Tingnan ang TIN guide namin.

- Proof of income — Pinakabagong 3-buwan na payslips, ITR, o Certificate of Employment na may compensation (para sa loan applications)

- Pag-IBIG MID Number + 24 buwanang contributions — Kailangan para sa Pag-IBIG housing loans. Tingnan ang Pag-IBIG guide namin.

- Marriage certificate (kung may asawa) — Kailangan ang pahintulot ng asawa para sa pagbili ng property sa ilalim ng Family Code

- Certified True Copy ng titulo (TCT/CCT) — Kinukuha sa Registry of Deeds para i-verify ang pagmamay-ari

- Updated na real property tax receipts — Patunay na nabayaran na ng seller ang lahat ng property taxes hanggang sa kasalukuyan

- Tax clearance mula sa Treasurer's Office — Nagkukumpirma na walang outstanding na property tax liabilities

Step-by-Step Process

Hakbang-Hakbang na Proseso

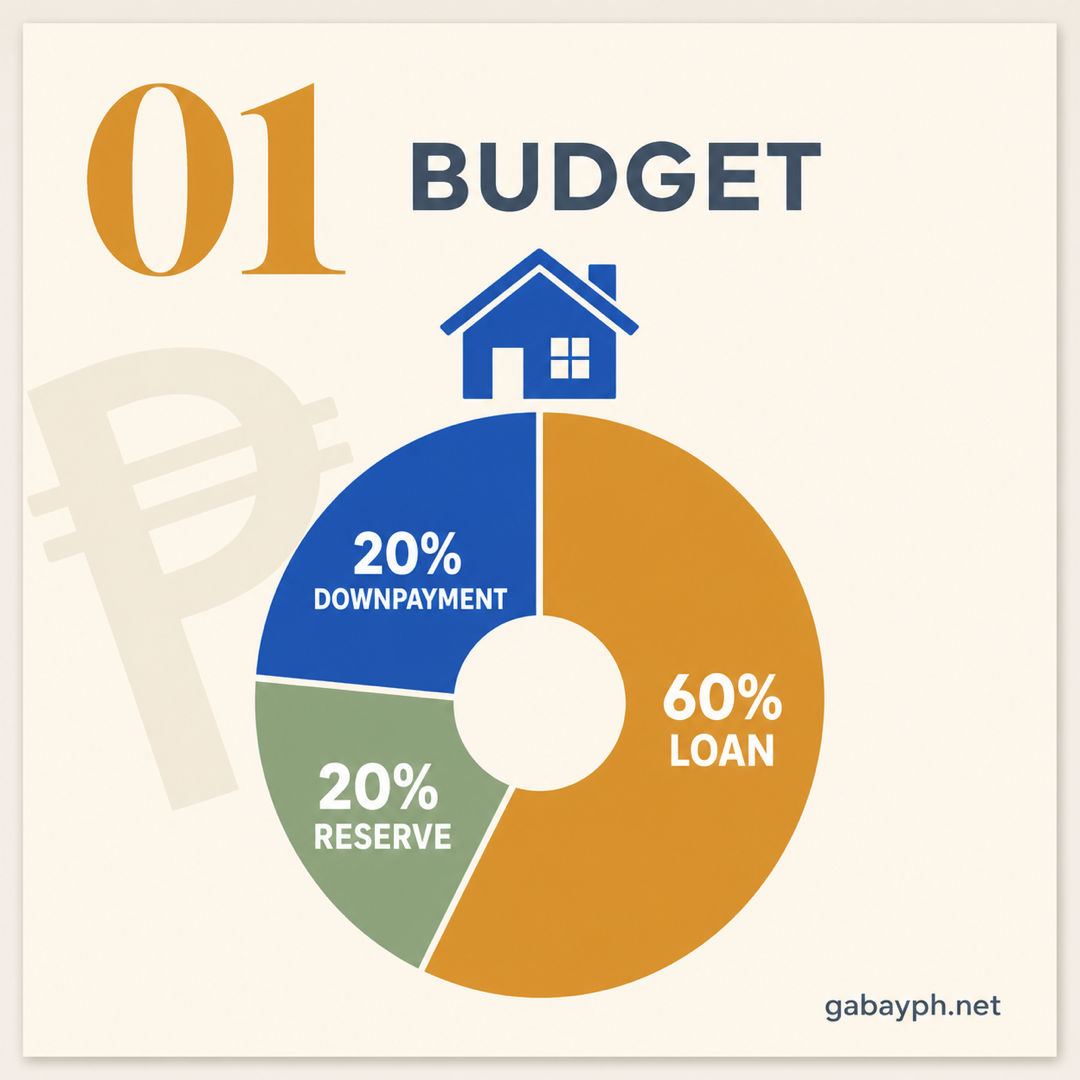

Assess Your Financial Readiness

Before house-hunting, get your finances in order:

- Save for the down payment — Typically 10-20% of the property price. For a ₱3 million property, that's ₱300,000-₱600,000. Also have 6 months of expenses in an emergency fund before buying.

- Know your borrowing limit — Monthly amortization should not exceed 30-35% of gross income. Clear existing debts first — banks check your debt-to-income ratio. Use our Loan Calculator to estimate payments.

- Check your Pag-IBIG contributions — You need at least 24 monthly contributions to qualify for a Pag-IBIG housing loan.

Research and Find Your Property

Start your search with clear criteria:

- Location — Consider proximity to your workplace, schools, hospitals, markets, and public transportation. Commuting costs add up significantly over 20-30 years.

- Property type — House and lot (TCT), condominium (CCT), or townhouse. Each has different price points, maintenance costs, and lifestyles.

- Budget range — Set a realistic total budget including down payment, closing costs (additional 5-8%), and move-in expenses.

- Where to look: Online listings (Lamudi.com.ph, Property24.com.ph, Carousell), developer websites, licensed real estate brokers, bank foreclosed properties (often 10-30% below market value), and Pag-IBIG acquired assets.

Verify the Property and Title

This is the most critical step — do NOT skip this:

- Get a Certified True Copy of the title from the Registry of Deeds (₱100-₱200 per copy). Compare it with the owner's copy to make sure they match.

- Check for liens and encumbrances — The title's annotations section will show any mortgages, adverse claims, or pending cases.

- Verify the tax declaration — Go to the local Assessor's Office and check that the property tax is current and the declared owner matches the title.

- Get a tax clearance from the Municipal/City Treasurer's Office confirming no outstanding property taxes.

- Inspect the property physically — Check for structural issues, flooding history, access to roads, water, and electricity.

- Hire a lawyer — A real estate lawyer (₱10,000-₱30,000) reviews documents, checks for legal issues, and protects your interest. This is NOT optional for private seller transactions.

I-assess ang Financial Readiness Mo

Bago maghanap ng bahay, ayusin muna ang finances mo:

- Mag-ipon para sa down payment — Karaniwang 10-20% ng presyo ng property. Para sa ₱3 milyon na property, iyan ay ₱300,000-₱600,000. Kailangan din ng 6 buwan na gastusin sa emergency fund bago bumili.

- Alamin ang borrowing limit mo — Hindi dapat lumampas sa 30-35% ng gross income ang buwanang amortization. Linisin muna ang mga utang — tinitignan ng mga bangko ang debt-to-income ratio. Gamitin ang aming Loan Calculator para i-estimate ang mga bayad.

- I-check ang Pag-IBIG contributions mo — Kailangan mo ng kahit 24 buwanang contributions para ma-qualify sa Pag-IBIG housing loan.

Mag-research at Maghanap ng Property

Simulan ang paghahanap mo na may malinaw na criteria:

- Lokasyon — Isaalang-alang ang proximity sa trabaho, mga paaralan, ospital, palengke, at pampublikong transportasyon. Ang gastos sa pagbibiyahe ay malaking-malaki sa loob ng 20-30 taon.

- Uri ng property — House and lot (TCT), condominium (CCT), o townhouse. Bawat isa ay may iba't ibang price points, maintenance costs, at lifestyles.

- Budget range — Mag-set ng realistikong kabuuang budget kasama ang down payment, closing costs (karagdagang 5-8%), at move-in expenses.

- Saan maghanap: Online listings (Lamudi.com.ph, Property24.com.ph, Carousell), developer websites, licensed real estate brokers, bank foreclosed properties (kadalasan 10-30% sa ilalim ng market value), at Pag-IBIG acquired assets.

I-verify ang Property at Titulo

Ito ang pinakamahalagang hakbang — HUWAG itong i-skip:

- Kumuha ng Certified True Copy ng titulo mula sa Registry of Deeds (₱100-₱200 bawat kopya). Ikumpara ito sa owner's copy para masigurong magkatugma ang mga ito.

- Mag-check ng liens at encumbrances — Ipapakita ng annotations section ng titulo ang anumang mortgages, adverse claims, o pending cases.

- I-verify ang tax declaration — Pumunta sa local Assessor's Office at i-check na updated ang property tax at tumutugma ang declared owner sa titulo.

- Kumuha ng tax clearance mula sa Municipal/City Treasurer's Office na nagkukumpirma na walang outstanding property taxes.

- I-inspect ang property nang personal — I-check kung may structural issues, flooding history, access sa kalsada, tubig, at kuryente.

- Kumuha ng abogado — Ang real estate lawyer (₱10,000-₱30,000) ang nagre-review ng mga dokumento, nag-che-check ng legal issues, at nagpoprotekta ng interes mo. HINDI ito opsyonal para sa private seller transactions.

Secure Your Financing

Once you've found and verified your property, apply for your housing loan:

- Pag-IBIG Housing Loan — Apply at the nearest Pag-IBIG Fund branch or online via the Virtual Pag-IBIG portal. Processing takes 20-30 business days. See detailed requirements in the Pag-IBIG section below.

- Bank Housing Loan — Apply at your preferred bank. Submit your documents, get pre-approved, then the bank will appraise the property. Processing takes 15-30 business days. See the bank comparison section below.

- In-house financing — Apply directly with the developer. Usually the fastest (1-7 days) but most expensive.

Get pre-approved first — Before making an offer on a property, get pre-approved for a loan. This tells you exactly how much you can borrow and shows the seller you're a serious buyer.

Execute the Deed of Sale and Pay

Once the loan is approved:

- Sign the Deed of Absolute Sale — Both buyer and seller sign before a notary public. This is the legal document that transfers ownership.

- Pay the down payment — Typically 10-20% of the property price, minus any reservation fees already paid.

- Pay closing costs — These include documentary stamp tax, transfer tax, registration fees, and notarial fees (see Transfer of Title section for details).

- Bank releases the loan — The bank or Pag-IBIG releases the loan proceeds to the seller (or developer).

Transfer the Title to Your Name

After the sale is completed, the title must be transferred to your name. This involves several government agencies and takes 2-6 months. See the detailed Transfer of Title section below for the complete process.

I-secure ang Financing Mo

Kapag nahanap at na-verify mo na ang property, mag-apply para sa housing loan mo:

- Pag-IBIG Housing Loan — Mag-apply sa pinakamalapit na Pag-IBIG Fund branch o online sa pamamagitan ng Virtual Pag-IBIG portal. Ang processing ay tumatagal ng 20-30 business days. Tingnan ang detalyadong requirements sa Pag-IBIG section sa ibaba.

- Bank Housing Loan — Mag-apply sa preferred na bangko mo. Isumite ang mga dokumento, ma-pre-approve, pagkatapos ia-appraise ng bangko ang property. Ang processing ay tumatagal ng 15-30 business days. Tingnan ang bank comparison section sa ibaba.

- In-house financing — Mag-apply direkta sa developer. Karaniwan ang pinakamabilis (1-7 araw) pero pinakamahal.

Ma-pre-approve muna — Bago gumawa ng offer sa property, kumuha muna ng pre-approval para sa loan. Sinasabi nito sa iyo kung eksaktong magkano ang maaari mong hiramin at ipinapakita sa seller na seryoso kang buyer.

I-execute ang Deed of Sale at Magbayad

Kapag na-approve na ang loan:

- Pirmahan ang Deed of Absolute Sale — Parehong buyer at seller ang pumipirma sa harap ng notary public. Ito ang legal na dokumento na naglilipat ng pagmamay-ari.

- Bayaran ang down payment — Karaniwang 10-20% ng presyo ng property, minus ang anumang reservation fees na nabayaran na.

- Bayaran ang closing costs — Kasama dito ang documentary stamp tax, transfer tax, registration fees, at notarial fees (tingnan ang Transfer of Title section para sa mga detalye).

- Ire-release ng bangko ang loan — Ire-release ng bangko o Pag-IBIG ang loan proceeds sa seller (o developer).

I-transfer ang Titulo sa Pangalan Mo

Pagkatapos makumpleto ang benta, kailangan i-transfer ang titulo sa pangalan mo. Kasangkot dito ang ilang government agencies at tumatagal ng 2-6 buwan. Tingnan ang detalyadong Transfer of Title section sa ibaba para sa kumpletong proseso.

Pag-IBIG Housing Loan

Pag-IBIG Housing Loan

The Pag-IBIG Fund (HDMF) housing loan is the most popular and affordable housing loan for Filipino workers. Here are the key details:

Eligibility

- Must be a Pag-IBIG member with at least 24 monthly contributions (need not be consecutive)

- Not more than 65 years old at loan maturity

- Must have the legal capacity to acquire and own real property

- Has no outstanding Pag-IBIG housing loan (only one at a time)

- Has not had a Pag-IBIG housing loan that was foreclosed, cancelled, or bought back within the last 5 years

Loan Limits and Terms

- Maximum loanable amount: ₱6,000,000

- Loan term: Up to 30 years

- Interest rates (2026):

- ₱500,000 and below: 5.375% per year

- ₱500,001 to ₱1,500,000: 6.375%

- ₱1,500,001 to ₱3,000,000: 7.375%

- ₱3,000,001 to ₱4,000,000: 8.375%

- ₱4,000,001 to ₱6,000,000: 10.375%

- Down payment: Minimum 10% (socialized housing may have lower down payment options)

- Processing time: 20-30 business days after complete submission

How to Apply

- Ensure you have at least 24 Pag-IBIG contributions

- Get a pre-qualification letter from any Pag-IBIG branch

- Find your property and negotiate terms with the seller

- Submit the Housing Loan Application (HLA) with required documents at any Pag-IBIG branch or via Virtual Pag-IBIG

- Pag-IBIG appraises the property and processes the loan

- Upon approval, sign the loan documents and Deed of Sale

Pro tip: If you're not yet a Pag-IBIG member, start contributing now. Even voluntary members and OFWs can qualify for the housing loan after 24 contributions.

Ang Pag-IBIG Fund (HDMF) housing loan ang pinakapopular at pinaka-affordable na housing loan para sa mga Pilipinong manggagawa. Narito ang mga pangunahing detalye:

Eligibility

- Dapat ay Pag-IBIG member na may kahit 24 buwanang contributions (hindi kailangang sunod-sunod)

- Hindi hihigit sa 65 taong gulang sa loan maturity

- Dapat may legal capacity na kumuha at magmay-ari ng real property

- Walang umiiral na Pag-IBIG housing loan (isa lang sa isang pagkakataon)

- Hindi nagkaroon ng Pag-IBIG housing loan na na-foreclose, na-cancel, o na-buy back sa loob ng huling 5 taon

Loan Limits at Terms

- Maximum loanable amount: ₱6,000,000

- Loan term: Hanggang 30 taon

- Interest rates (2026):

- ₱500,000 at pababa: 5.375% kada taon

- ₱500,001 hanggang ₱1,500,000: 6.375%

- ₱1,500,001 hanggang ₱3,000,000: 7.375%

- ₱3,000,001 hanggang ₱4,000,000: 8.375%

- ₱4,000,001 hanggang ₱6,000,000: 10.375%

- Down payment: Minimum 10% (ang socialized housing ay maaaring may mas mababang down payment options)

- Processing time: 20-30 business days pagkatapos ng kumpletong submission

Paano Mag-apply

- Siguraduhing mayroon kang kahit 24 Pag-IBIG contributions

- Kumuha ng pre-qualification letter mula sa kahit anong Pag-IBIG branch

- Hanapin ang property mo at makipag-negotiate ng terms sa seller

- Isumite ang Housing Loan Application (HLA) kasama ang required documents sa kahit anong Pag-IBIG branch o sa pamamagitan ng Virtual Pag-IBIG

- Ia-appraise ng Pag-IBIG ang property at ipoproseso ang loan

- Sa pag-approve, pirmahan ang loan documents at Deed of Sale

Pro tip: Kung hindi ka pa Pag-IBIG member, magsimulang mag-contribute ngayon. Kahit ang voluntary members at OFWs ay maaaring mag-qualify sa housing loan pagkatapos ng 24 contributions.

Bank Housing Loans Compared

Mga Bank Housing Loan na Pinaghahambing

If you need more than ₱6 million (Pag-IBIG's cap) or want faster processing, consider a bank housing loan. Here's how the major banks compare:

BPI Housing Loan

- Fixed rate: 6.5-7.5% for the first 3-5 years, then repricing based on market rates

- Maximum loan: Up to 80% of appraised value (90% for some developer tie-ups)

- Term: Up to 20 years

- Minimum income: ₱50,000/month gross

- Processing: 15-20 business days

BDO Housing Loan

- Fixed rate: 6.75-8.0% for the first 3-5 years, then annual repricing

- Maximum loan: Up to 80% of appraised value

- Term: Up to 20 years

- Minimum income: ₱40,000/month gross

- Processing: 15-25 business days

- Advantage: Largest branch network, many developer partners

Metrobank Housing Loan

- Fixed rate: 6.5-7.75% for the first 3-5 years

- Maximum loan: Up to 80% of appraised value

- Term: Up to 20 years

- Minimum income: ₱40,000/month gross

- Processing: 15-20 business days

Important notes: All bank rates listed are the initial fixed rates. After the fixed period ends (usually 3-5 years), the rate "reprices" based on market conditions and may increase. Always ask about the repricing mechanism and compare the total cost of borrowing over the full loan term, not just the initial rate. Use our Loan Calculator to compare monthly payments across different rates and terms.

Kung kailangan mo ng higit sa ₱6 milyon (cap ng Pag-IBIG) o gusto mo ng mas mabilis na processing, isaalang-alang ang bank housing loan. Narito kung paano nagkukumpara ang mga pangunahing bangko:

BPI Housing Loan

- Fixed rate: 6.5-7.5% para sa unang 3-5 taon, pagkatapos ay repricing batay sa market rates

- Maximum loan: Hanggang 80% ng appraised value (90% para sa ilang developer tie-ups)

- Term: Hanggang 20 taon

- Minimum income: ₱50,000/buwan gross

- Processing: 15-20 business days

BDO Housing Loan

- Fixed rate: 6.75-8.0% para sa unang 3-5 taon, pagkatapos ay annual repricing

- Maximum loan: Hanggang 80% ng appraised value

- Term: Hanggang 20 taon

- Minimum income: ₱40,000/buwan gross

- Processing: 15-25 business days

- Advantage: Pinakamalawak na branch network, maraming developer partners

Metrobank Housing Loan

- Fixed rate: 6.5-7.75% para sa unang 3-5 taon

- Maximum loan: Hanggang 80% ng appraised value

- Term: Hanggang 20 taon

- Minimum income: ₱40,000/buwan gross

- Processing: 15-20 business days

Mahahalagang tala: Lahat ng bank rates na nakalista ay ang initial fixed rates. Pagkatapos matapos ang fixed period (karaniwan 3-5 taon), ang rate ay "nagrere-reprice" batay sa market conditions at maaaring tumaas. Palaging itanong ang repricing mechanism at ikumpara ang kabuuang halaga ng paghiram sa buong loan term, hindi lang ang initial rate. Gamitin ang aming Loan Calculator para ikumpara ang buwanang bayad sa iba't ibang rates at terms.

How to Check for Liens at Registry of Deeds

Paano Mag-check ng Liens sa Registry of Deeds

Checking for liens is one of the most important steps in buying a property. Here's exactly how to do it:

- Go to the Registry of Deeds in the city or province where the property is located. Bring the property's title number (e.g., TCT No. 12345) and the owner's name.

- Request a Certified True Copy of the title — Pay the fee (₱100-₱200). The certified copy is an official reproduction of the title as it exists in the Registry's records.

- Check the Annotations/Encumbrances section — This is on the back of the title. Look for:

- Mortgage annotations — If the property is currently mortgaged to a bank, it will be listed here. The mortgage must be cancelled (paid off) before the sale.

- Adverse claims — Someone else claiming ownership of the property.

- Lis pendens — A court case involving the property is pending.

- Attachments or levies — The property has been seized as security for a debt or court judgment.

- Previous sales or cancellations — History of ownership transfers.

- Compare with the owner's copy — The seller should have an "Owner's Duplicate Copy" of the title. Compare it page-by-page with the Registry's Certified True Copy. They should be identical. If there are discrepancies, this is a major red flag.

If you find any liens or encumbrances: Do NOT proceed with the purchase until they are resolved. Consult a real estate lawyer immediately.

Ang pag-check ng liens ay isa sa pinakamahalgang hakbang sa pagbili ng property. Narito ang eksaktong paraan kung paano ito gawin:

- Pumunta sa Registry of Deeds sa lungsod o lalawigan kung saan matatagpuan ang property. Dalhin ang title number ng property (hal., TCT No. 12345) at ang pangalan ng may-ari.

- Humiling ng Certified True Copy ng titulo — Bayaran ang bayad (₱100-₱200). Ang certified copy ay opisyal na reproduction ng titulo ayon sa records ng Registry.

- I-check ang Annotations/Encumbrances section — Ito ay nasa likod ng titulo. Hanapin ang:

- Mortgage annotations — Kung ang property ay kasalukuyang naka-mortgage sa bangko, ililista ito dito. Ang mortgage ay kailangan i-cancel (bayaran) bago ang benta.

- Adverse claims — May ibang tao na nag-claim ng pagmamay-ari ng property.

- Lis pendens — May pending na kaso sa korte na kinasasangkutan ng property.

- Attachments o levies — Ang property ay kinuha bilang seguridad para sa utang o court judgment.

- Mga nakaraang benta o cancellations — Kasaysayan ng mga ownership transfers.

- Ikumpara sa owner's copy — Ang seller ay dapat may "Owner's Duplicate Copy" ng titulo. Ikumpara ito pahina-pahina sa Certified True Copy ng Registry. Dapat magkatugma ang mga ito. Kung may mga pagkakaiba, ito ay malaking red flag.

Kung may nakita kang liens o encumbrances: HUWAG magpatuloy sa pagbili hanggang hindi nalulutas ang mga ito. Kumonsulta kaagad sa real estate lawyer.

Transfer of Title Process

Proseso ng Transfer ng Titulo

After the sale is completed, you need to transfer the property title to your name. This involves the following steps and costs:

- Pay Capital Gains Tax (CGT) at BIR — 6% of the selling price or zonal value (whichever is higher). Paid by the seller (but often negotiated). Must be paid within 30 days of the sale.

- Pay Documentary Stamp Tax (DST) at BIR — 1.5% of the selling price or zonal value (whichever is higher). Usually paid by the buyer.

- Get a Certificate Authorizing Registration (CAR) from BIR — After paying CGT and DST, the BIR issues a CAR. Processing takes about 5-15 business days.

- Pay Transfer Tax at the Treasurer's Office — 0.5-0.75% of the selling price or zonal value (varies by city/municipality).

- Pay Registration Fee at the Registry of Deeds — Based on a sliding scale (approximately 0.25-0.5% of the property value). Submit the Deed of Sale, CAR, tax receipts, and old title.

- Registry of Deeds issues a new TCT/CCT in your name — Processing takes 1-3 months.

- Update the Tax Declaration at the Assessor's Office — Bring the new title and have the tax declaration updated to your name.

Estimated Closing Costs Summary

For a ₱3,000,000 property:

- Capital Gains Tax (6%): ₱180,000 (seller's responsibility, but negotiate)

- Documentary Stamp Tax (1.5%): ₱45,000

- Transfer Tax (0.5-0.75%): ₱15,000-₱22,500

- Registration Fee: ₱7,500-₱15,000

- Notarial Fee: ₱10,000-₱30,000

- Total buyer closing costs: approximately ₱77,500-₱112,500 (2.5-3.75% of property price)

Pagkatapos makumpleto ang benta, kailangan mong i-transfer ang titulo ng property sa pangalan mo. Kasama dito ang mga sumusunod na hakbang at gastos:

- Magbayad ng Capital Gains Tax (CGT) sa BIR — 6% ng selling price o zonal value (alinman ang mas mataas). Binabayaran ng seller (pero madalas na pinag-uusapan). Kailangan bayaran sa loob ng 30 araw mula sa benta.

- Magbayad ng Documentary Stamp Tax (DST) sa BIR — 1.5% ng selling price o zonal value (alinman ang mas mataas). Karaniwang binabayaran ng buyer.

- Kumuha ng Certificate Authorizing Registration (CAR) mula sa BIR — Pagkatapos magbayad ng CGT at DST, maglalabas ang BIR ng CAR. Ang processing ay tumatagal ng mga 5-15 business days.

- Magbayad ng Transfer Tax sa Treasurer's Office — 0.5-0.75% ng selling price o zonal value (iba-iba sa bawat lungsod/munisipalidad).

- Magbayad ng Registration Fee sa Registry of Deeds — Batay sa sliding scale (humigit-kumulang 0.25-0.5% ng property value). Isumite ang Deed of Sale, CAR, tax receipts, at lumang titulo.

- Maglalabas ang Registry of Deeds ng bagong TCT/CCT sa pangalan mo — Ang processing ay tumatagal ng 1-3 buwan.

- I-update ang Tax Declaration sa Assessor's Office — Dalhin ang bagong titulo at ipa-update ang tax declaration sa pangalan mo.

Estimated na Buod ng Closing Costs

Para sa ₱3,000,000 na property:

- Capital Gains Tax (6%): ₱180,000 (responsibilidad ng seller, pero i-negotiate)

- Documentary Stamp Tax (1.5%): ₱45,000

- Transfer Tax (0.5-0.75%): ₱15,000-₱22,500

- Registration Fee: ₱7,500-₱15,000

- Notarial Fee: ₱10,000-₱30,000

- Kabuuang buyer closing costs: humigit-kumulang ₱77,500-₱112,500 (2.5-3.75% ng presyo ng property)

Real Property Tax Basics

Basics ng Real Property Tax

Once you own a property, you're responsible for paying real property tax (RPT) every year. Here's what you need to know:

- RPT rate: Depends on your location. In Metro Manila, it's 2% of the assessed value. In provinces, it's 1% of the assessed value.

- Assessed value vs market value: The assessed value is a fraction of the market value. For residential properties, the assessment level is typically 20% of the market value. So a property with a market value of ₱3,000,000 would have an assessed value of ₱600,000.

- Annual RPT example: ₱3,000,000 property in Metro Manila = ₱600,000 assessed value x 2% = ₱12,000/year.

- When to pay: RPT is due every January. You can pay in full (some cities give a 10-20% early payment discount) or quarterly (March, June, September, December).

- Where to pay: At the City/Municipal Treasurer's Office or online (some cities like Quezon City, Makati, and Pasig offer online RPT payment).

- Penalty for late payment: 2% per month on the unpaid amount, up to a maximum of 72% (36 months).

- Special Education Fund (SEF): An additional 1% of assessed value is added to your RPT bill for education funding.

Kapag nagmamay-ari ka na ng property, responsable ka sa pagbabayad ng real property tax (RPT) bawat taon. Narito ang kailangan mong malaman:

- RPT rate: Depende sa lokasyon mo. Sa Metro Manila, ito ay 2% ng assessed value. Sa mga lalawigan, ito ay 1% ng assessed value.

- Assessed value vs market value: Ang assessed value ay isang fraction ng market value. Para sa residential properties, ang assessment level ay karaniwang 20% ng market value. Kaya ang property na may market value na ₱3,000,000 ay magkakaroon ng assessed value na ₱600,000.

- Halimbawa ng taunang RPT: ₱3,000,000 na property sa Metro Manila = ₱600,000 assessed value x 2% = ₱12,000/taon.

- Kailan magbabayad: Ang RPT ay due bawat Enero. Pwede kang magbayad nang buo (may 10-20% early payment discount ang ibang lungsod) o quarterly (Marso, Hunyo, Setyembre, Disyembre).

- Saan magbabayad: Sa City/Municipal Treasurer's Office o online (ang ilang lungsod tulad ng Quezon City, Makati, at Pasig ay nag-o-offer ng online RPT payment).

- Multa sa late payment: 2% bawat buwan sa hindi nabayarang halaga, hanggang maximum na 72% (36 buwan).

- Special Education Fund (SEF): Isang karagdagang 1% ng assessed value ang idinaragdag sa RPT bill mo para sa education funding.

Common Scams to Avoid

Mga Karaniwang Scam na Dapat Iwasan

- Fake titles — Forged or tampered land titles. Always get a Certified True Copy from the Registry of Deeds and compare it with the seller's copy. Have a lawyer verify authenticity.

- Double sale — The seller sells the same property to multiple buyers simultaneously. Check the title for recent annotations and ensure no other transactions are pending.

- Selling without authority — Someone selling a property they don't actually own or don't have the authority to sell (e.g., a relative selling without a Special Power of Attorney). Always verify the seller's identity matches the title holder.

- "Clean title" that isn't clean — Seller claims no liens, but the title has annotations showing mortgages, adverse claims, or pending cases. This is why you must check the Registry's copy, not just the seller's copy.

- Unlicensed developers — Developers selling pre-selling units without a License to Sell from DHSUD. They may never complete construction. Verify at dhsud.gov.ph.

- Cash-only deals with no documentation — Never pay large sums without a proper Deed of Sale, official receipts, and notarization. Handshake deals on property are a recipe for disaster.

- Overpriced appraisals — Some sellers inflate the property's value. Get an independent appraisal from a licensed appraiser, not one recommended by the seller.

- Agent collecting directly — Legitimate real estate agents and brokers never collect payments. All payments should go directly to the seller, developer, or escrow account. If an agent asks you to pay them, that's a red flag.

- Pekeng titulo — Peke o tinempeng land titles. Palaging kumuha ng Certified True Copy mula sa Registry of Deeds at ikumpara ito sa kopya ng seller. Ipasuri sa abogado ang authenticity.

- Double sale — Ibinebenta ng seller ang parehong property sa maraming buyers nang sabay-sabay. I-check ang titulo para sa mga recent annotations at siguraduhing walang ibang mga transaction na pending.

- Pagbebenta nang walang awtoridad — May ibang tao na nagbebenta ng property na hindi naman talaga kanila o walang awtoridad na ibenta (hal., kamag-anak na nagbebenta nang walang Special Power of Attorney). Palaging i-verify na ang identity ng seller ay tumutugma sa title holder.

- "Clean title" na hindi pala clean — Inaangkin ng seller na walang liens, pero ang titulo ay may mga annotation na nagpapakita ng mortgages, adverse claims, o pending cases. Kaya kailangan mong i-check ang kopya ng Registry, hindi lang ang kopya ng seller.

- Mga unlicensed developers — Mga developer na nagbebenta ng pre-selling units nang walang License to Sell mula sa DHSUD. Maaaring hindi nila kailanman makumpleto ang konstruksyon. I-verify sa dhsud.gov.ph.

- Cash-only deals na walang dokumentasyon — Huwag kailanman magbayad ng malalaking halaga nang walang tamang Deed of Sale, official receipts, at notarization. Ang mga handshake deals sa property ay paghahanda para sa sakuna.

- Overpriced appraisals — Ang ibang sellers ay nagpapalaki ng value ng property. Kumuha ng independent appraisal mula sa licensed appraiser, hindi isa na inirerekomenda ng seller.

- Agent na direktang nangongolekta — Ang mga lehitimong real estate agents at brokers ay hindi kailanman nangongolekta ng bayad. Lahat ng bayad ay dapat diretso sa seller, developer, o escrow account. Kung hiningi ng agent na bayaran sila, red flag iyan.

Pro Tips

Mga Payo

- Start saving and contributing to Pag-IBIG NOW — Even if you're years away from buying, start your 24-month contribution clock. It costs as little as ₱200/month. See our Pag-IBIG guide.

- Always hire a lawyer for private seller transactions — The ₱10,000-₱30,000 fee is tiny compared to the risk of buying a property with title problems that could cost you millions.

- Don't skip the Registry of Deeds check — This 30-minute trip and ₱200 fee could save you from the biggest financial mistake of your life.

- Consider bank foreclosed properties — Banks sell foreclosed properties at 10-30% below market value. Check BPI, BDO, and Metrobank websites for listings. These are generally safe since the bank has already verified the titles.

- Factor in ALL costs — Beyond the purchase price, budget for: closing costs (5-8%), renovation/repairs, moving expenses, furniture, and your first 6 months of amortization payments. Use our Loan Calculator.

- Location over aesthetics — You can renovate an ugly house, but you can't move it closer to your workplace. Prioritize commute time, flood risk, and neighborhood safety over fancy finishes.

- Visit the property at different times — Go during morning rush hour (to test the commute), during heavy rain (to check for flooding), and at night (to assess safety and noise).

- Never sign anything you don't fully understand — If the Deed of Sale, loan documents, or any contract has terms you don't understand, ask your lawyer to explain before signing.

- Magsimulang mag-ipon at mag-contribute sa Pag-IBIG NGAYON — Kahit maraming taon ka pa bago bumili, simulan na ang 24-buwan na contribution clock mo. Kasing mura lang ng ₱200/buwan. Tingnan ang Pag-IBIG guide namin.

- Palaging kumuha ng abogado para sa private seller transactions — Ang ₱10,000-₱30,000 na bayad ay napakaliit kumpara sa panganib na bumili ng property na may title problems na maaaring magastos ng milyun-milyon.

- Huwag i-skip ang Registry of Deeds check — Ang 30-minutong pagbisita at ₱200 na bayad na ito ay maaaring iligtas ka mula sa pinakamalaking financial mistake ng buhay mo.

- Isaalang-alang ang bank foreclosed properties — Nagbebenta ang mga bangko ng foreclosed properties sa 10-30% na mas mababa sa market value. I-check ang BPI, BDO, at Metrobank websites para sa listings. Ang mga ito ay karaniwan ligtas dahil na-verify na ng bangko ang mga titulo.

- I-factor in ang LAHAT ng gastos — Bukod sa purchase price, mag-budget para sa: closing costs (5-8%), renovation/repairs, moving expenses, furniture, at unang 6 buwan ng amortization payments. Gamitin ang aming Loan Calculator.

- Lokasyon kaysa aesthetics — Pwede mong i-renovate ang pangit na bahay, pero hindi mo ito mailalapit sa trabaho mo. Unahin ang commute time, flood risk, at kaligtasan ng neighborhood kaysa sa magagandang finishes.

- Bisitahin ang property sa iba't ibang oras — Pumunta sa morning rush hour (para subukan ang commute), habang malakas ang ulan (para i-check ang pagbaha), at sa gabi (para i-assess ang kaligtasan at ingay).

- Huwag kailanman pumirma ng anumang hindi mo ganap na naiintindihan — Kung ang Deed of Sale, loan documents, o anumang kontrata ay may mga terminong hindi mo naiintindihan, sabihan ang abogado mo na ipaliwanag bago pumirma.

Frequently Asked Questions

Mga Madalas Itanong

How much money do I need to buy a house?

At minimum, you need: down payment (10-20% of property price) + closing costs (5-8%) + emergency fund (6 months of expenses). For a ₱3,000,000 property, that means: ₱300,000-₱600,000 (down payment) + ₱150,000-₱240,000 (closing costs) + your emergency fund = roughly ₱500,000-₱900,000 in savings before buying. Some developers offer lower down payments (5-10%), but lower down payment means higher monthly amortization.

Magkano ang kailangan kong pera para bumili ng bahay?

Sa pinakamababa, kailangan mo ng: down payment (10-20% ng presyo ng property) + closing costs (5-8%) + emergency fund (6 buwan na gastusin). Para sa ₱3,000,000 na property, ibig sabihin: ₱300,000-₱600,000 (down payment) + ₱150,000-₱240,000 (closing costs) + emergency fund mo = humigit-kumulang ₱500,000-₱900,000 na ipon bago bumili. Ang ibang developers ay nag-o-offer ng mas mababang down payments (5-10%), pero ang mas mababang down payment ay nangangahulugang mas mataas na buwanang amortization.

Which is better: Pag-IBIG or bank housing loan?

Pag-IBIG is better for most first-time buyers because of its lower interest rates (5.375-10.375% vs 6.5-10%+ for banks) and longer repayment terms (up to 30 years vs 20 years for most banks). However, bank loans are better if: you need more than ₱6 million, you want faster processing, or you don't have 24 months of Pag-IBIG contributions yet. Some buyers use both — a Pag-IBIG loan for the main amount and a bank loan for the balance above ₱6 million.

Alin ang mas maganda: Pag-IBIG o bank housing loan?

Mas maganda ang Pag-IBIG para sa karamihan ng first-time buyers dahil sa mas mababang interest rates nito (5.375-10.375% vs 6.5-10%+ para sa mga bangko) at mas mahabang repayment terms (hanggang 30 taon vs 20 taon para sa karamihan ng mga bangko). Gayunpaman, mas maganda ang bank loans kung: kailangan mo ng higit sa ₱6 milyon, gusto mo ng mas mabilis na processing, o wala ka pang 24 buwan na Pag-IBIG contributions. Ang ilang buyers ay gumagamit ng pareho — Pag-IBIG loan para sa pangunahing halaga at bank loan para sa balance na higit sa ₱6 milyon.

Can OFWs buy property in the Philippines?

Yes! Filipino citizens, including OFWs, can buy any type of property (house and lot, condo, land) in the Philippines. OFWs can also apply for Pag-IBIG housing loans as long as they have at least 24 monthly contributions and meet the other requirements. Many OFWs appoint a trusted family member via Special Power of Attorney (SPA) to handle the purchase and paperwork on their behalf.

Pwede bang bumili ng property sa Pilipinas ang mga OFW?

Oo! Ang mga Filipino citizens, kasama ang mga OFW, ay maaaring bumili ng kahit anong uri ng property (house and lot, condo, lupa) sa Pilipinas. Ang mga OFW ay maaari ring mag-apply para sa Pag-IBIG housing loans basta may kahit 24 buwanang contributions sila at natutugunan ang ibang mga requirements. Maraming OFW ang nagtatalaga ng pinagkakatiwalaang miyembro ng pamilya sa pamamagitan ng Special Power of Attorney (SPA) para pangasiwaan ang pagbili at paperwork sa kanilang behalf.

What is the difference between TCT and tax declaration?

A TCT (Transfer Certificate of Title) is the official proof of land ownership registered at the Registry of Deeds. It is the strongest evidence of ownership recognized by law. A Tax Declaration is only a record at the local Assessor's Office showing who is paying property taxes on a piece of land — it does NOT prove ownership. Many families in the Philippines possess only tax declarations but no title. Buying property based solely on a tax declaration is extremely risky because the "owner" may not have legal ownership.

Ano ang pagkakaiba ng TCT at tax declaration?

Ang TCT (Transfer Certificate of Title) ay ang opisyal na patunay ng pagmamay-ari ng lupa na nakarehistro sa Registry of Deeds. Ito ang pinakamalakas na ebidensya ng pagmamay-ari na kinikilala ng batas. Ang Tax Declaration ay isang record lang sa local Assessor's Office na nagpapakita kung sino ang nagbabayad ng property taxes sa isang piraso ng lupa — HINDI ito nagpapatunay ng pagmamay-ari. Maraming pamilya sa Pilipinas ang may tax declarations lang pero walang titulo. Ang pagbili ng property batay lang sa tax declaration ay sobrang mapanganib dahil maaaring walang legal na pagmamay-ari ang "may-ari."

How long does the entire home buying process take?

From start to finish, expect the process to take 3-6 months: property search and evaluation (2-8 weeks), loan application and approval (3-6 weeks), signing and payment (1-2 weeks), and title transfer (2-6 months). The title transfer is the longest part and involves multiple government agencies. Buying from a developer is generally faster because they handle much of the paperwork.

Gaano katagal ang buong proseso ng pagbili ng bahay?

Mula simula hanggang katapusan, asahan na ang proseso ay tatagal ng 3-6 buwan: paghahanap at pag-evaluate ng property (2-8 linggo), loan application at approval (3-6 linggo), pagpirma at pagbabayad (1-2 linggo), at title transfer (2-6 buwan). Ang title transfer ang pinakamahabang bahagi at kinabibilangan ng maraming government agencies. Ang pagbili mula sa developer ay karaniwan mas mabilis dahil hinahawakan nila ang karamihan ng paperwork.