How to Create a Household Budget in the Philippines (2026 Guide)

Paano Gumawa ng Budget sa Bahay sa Pilipinas (2026 Gabay)

5 Things to Know

Household budget in five facts.

Quick Summary

Mabilis na Buod

Important Disclaimer

This guide is for educational purposes only and does not constitute financial advice. Individual circumstances vary. Consult a licensed financial advisor for personalized guidance.

Mahalagang Disclaimer

Ang gabay na ito ay para sa layuning pang-edukasyon lamang at hindi bumubuo ng financial advice. Iba-iba ang sitwasyon ng bawat tao. Kumonsulta sa isang lisensyadong financial advisor para sa personalized na gabay.

Table of Contents

Talaan ng Nilalaman

- Bakit Mag-budget?

- Mga Kakailanganin Mo Bago Magsimula

- Mga Template ng Budget Ayon sa Kita

- Ang Filipino 50/30/20 Rule na Adjusted

- Pag-track ng mga Gastos Mo

- Palengke vs Supermarket

- Pagbawas ng Buwanang Gastos

- Pag-manage ng Utang at Paluwagan

- Pag-iipon Kahit Mahigpit ang Budget

- Mga Payo

- Mga Madalas Itanong

Why Budget? Bakit Kailangan Mag-budget?

Bakit Kailangan Mag-budget?

Roughly 7 out of 10 Filipino families live paycheck to paycheck. A household budget isn't about deprivation — it's about knowing where your money goes. Even a simple budget on paper can help you:

Mga 7 sa 10 pamilyang Pilipino ang nabubuhay nang paycheck to paycheck. Ang household budget ay hindi tungkol sa paghihigpit — ito ay tungkol sa pag-alam kung saan napupunta ang pera mo. Kahit simpleng budget sa papel, makakatulong ito sa iyo na:

- Avoid being "isang kahig, isang tuka" — Stop the cycle of running out before the next payday

- Build an emergency fund — Even small amounts add up over time

- Reduce stress about money — When you have a plan, hindi ka laging nag-aalala

- Reach financial goals — Whether it's a new appliance, tuition, or a family vacation

- Avoid falling into debt traps — Less reliance on 5-6 and informal lending

- Iwasan ang "isang kahig, isang tuka" — Tapusin ang cycle ng pag-ubos ng pera bago ang susunod na sweldo

- Mag-build ng emergency fund — Kahit maliit na halaga, naiipon din kapag pinagsama-sama

- Mabawasan ang stress tungkol sa pera — Kapag may plano ka, hindi ka laging nag-aalala

- Maabot ang mga financial goals — Whether bagong appliance, tuition, o family vacation

- Maiwasan ang mga debt traps — Mas konting pag-asa sa 5-6 at informal lending

The good news? You don't need fancy software or a finance degree. Kailangan mo lang ng konting oras, isang notebook (or your phone), and the willingness to be honest about your spending habits. Let's get started.

Ang magandang balita? Hindi mo kailangan ng magarang software o finance degree. Kailangan mo lang ng konting oras, isang notebook (o phone mo), at ang kahandaang maging honest tungkol sa spending habits mo. Tara, simulan na natin.

What You Need Before Starting

- Your monthly income records — Pay slips, business earnings, remittance records, or any regular income source

- List of monthly bills — Rent, electricity, water, internet, phone, insurance, loan payments

- Receipts or notes of daily spending — Even rough estimates of food, transpo, and miscellaneous expenses for the past month

- A notebook, spreadsheet, or phone app — Anything you'll actually use consistently to track expenses

Mga Kakailanganin Mo Bago Magsimula

- Mga record ng buwanang kita mo — Pay slips, kita sa negosyo, padala, o kahit anong regular na source of income

- Listahan ng buwanang bills — Renta, kuryente, tubig, internet, phone, insurance, bayad sa utang

- Mga resibo o notes ng pang-araw-araw na gastos — Kahit rough estimates ng pagkain, pamasahe, at ibang gastos noong nakaraang buwan

- Notebook, spreadsheet, o phone app — Kahit ano basta gagamitin mo consistently para i-track ang gastos

Budget Templates by Income Level

Mga Template ng Budget Ayon sa Kita

Below are sample monthly budgets for three common household income levels in the Philippines. These are starting points — adjust based on your family's actual needs. Ang key dito is every peso has a job.

Family Earning ~₱15,000/month

This is common for minimum-wage earners in the provinces or entry-level workers sa NCR na nag-ro-room sharing. Tight, pero kayang i-budget:

- Rent/housing: ₱4,000 (room, boarding house, or shared apartment)

- Food: ₱5,000 (roughly ₱165/day for the family — palengke-focused shopping)

- Utilities (kuryente, tubig): ₱1,500

- Transportation: ₱1,500 (jeepney, tricycle, or bike commute)

- Savings/emergency: ₱1,000 (target: kahit ₱250/week lang, unahin ito)

- Miscellaneous: ₱2,000 (load, school needs, toiletries, medicine)

Total: ₱15,000. Very tight, pero the key is prioritizing needs first. Kahit maliit ang savings, the habit matters more than the amount.

Family Earning ~₱25,000/month

More breathing room. This is around the median household income in Metro Manila:

- Rent/housing: ₱6,000 (small apartment or condo share)

- Food: ₱7,000 (₱230/day — mix of palengke and occasional supermarket)

- Utilities: ₱2,500 (electricity, water, internet bundle)

- Transportation: ₱2,500 (daily commute, occasional Grab for emergencies)

- Savings/emergency: ₱3,000 (₱750/week — build your EF first)

- Insurance/SSS/Pag-IBIG: ₱1,000 (voluntary contributions if applicable)

- Miscellaneous: ₱3,000 (load, entertainment, toiletries, school supplies)

Total: ₱25,000. You can start building a proper emergency fund at this income level. Target: 3 months' worth of expenses saved.

Family Earning ~₱50,000/month

Comfortable but still requires discipline. Mas malaki ang temptation to lifestyle-inflate:

- Rent/housing: ₱12,000 (decent apartment or condo unit)

- Food: ₱10,000 (₱330/day — palengke, supermarket, occasional restaurant)

- Utilities: ₱4,000 (electricity, water, internet, phone plan)

- Transportation: ₱4,000 (commute, gas if may sasakyan, Grab)

- Savings/investments: ₱10,000 (EF, MP2, stocks, mutual funds)

- Insurance/SSS/Pag-IBIG/PhilHealth: ₱2,000

- Children's education fund: ₱3,000

- Miscellaneous/wants: ₱5,000 (entertainment, dining out, shopping, subscriptions)

Total: ₱50,000. At this level, you should be aggressively building savings AND investing. Don't let lifestyle creep eat the extra income.

Nasa ibaba ang mga sample na buwanang budget para sa tatlong karaniwang income level ng mga household sa Pilipinas. Mga starting point lang ito — i-adjust ayon sa aktwal na pangangailangan ng pamilya mo. Ang key dito ay bawat piso may trabaho.

Pamilyang Kumikita ng ~₱15,000/buwan

Karaniwan ito para sa mga minimum-wage earners sa probinsya o entry-level workers sa NCR na nag-ro-room sharing. Mahigpit, pero kayang i-budget:

- Renta/tirahan: ₱4,000 (kwarto, boarding house, o shared apartment)

- Pagkain: ₱5,000 (mga ₱165/araw para sa pamilya — palengke-focused na pamimili)

- Utilities (kuryente, tubig): ₱1,500

- Pamasahe: ₱1,500 (jeepney, tricycle, o bike commute)

- Ipon/emergency: ₱1,000 (target: kahit ₱250/linggo lang, unahin ito)

- Iba pa: ₱2,000 (load, pang-eskwela, toiletries, gamot)

Kabuuan: ₱15,000. Sobrang higpit, pero ang susi ay unahin ang mga pangangailangan. Kahit maliit ang ipon, mas mahalaga ang habit kaysa sa halaga.

Pamilyang Kumikita ng ~₱25,000/buwan

May mas konting breathing room. Malapit ito sa median household income sa Metro Manila:

- Renta/tirahan: ₱6,000 (maliit na apartment o condo share)

- Pagkain: ₱7,000 (₱230/araw — halo-halong palengke at paminsan-minsang supermarket)

- Utilities: ₱2,500 (kuryente, tubig, internet bundle)

- Pamasahe: ₱2,500 (pang-araw-araw na commute, paminsan-minsang Grab para sa emergency)

- Ipon/emergency: ₱3,000 (₱750/linggo — unahin muna ang EF)

- Insurance/SSS/Pag-IBIG: ₱1,000 (voluntary contributions kung applicable)

- Iba pa: ₱3,000 (load, entertainment, toiletries, school supplies)

Kabuuan: ₱25,000. Sa income level na ito, pwede ka nang mag-build ng maayos na emergency fund. Target: 3 buwang halaga ng expenses na naka-save.

Pamilyang Kumikita ng ~₱50,000/buwan

Komportable na pero kailangan pa rin ng disiplina. Mas malaki ang temptation to lifestyle-inflate:

- Renta/tirahan: ₱12,000 (disenteng apartment o condo unit)

- Pagkain: ₱10,000 (₱330/araw — palengke, supermarket, paminsan-minsang restaurant)

- Utilities: ₱4,000 (kuryente, tubig, internet, phone plan)

- Pamasahe: ₱4,000 (commute, gas kung may sasakyan, Grab)

- Ipon/investments: ₱10,000 (EF, MP2, stocks, mutual funds)

- Insurance/SSS/Pag-IBIG/PhilHealth: ₱2,000

- Pondo sa edukasyon ng mga anak: ₱3,000

- Miscellaneous/gusto: ₱5,000 (entertainment, kain sa labas, shopping, subscriptions)

Kabuuan: ₱50,000. Sa level na ito, dapat aggressive ka na sa pag-iipon AT pag-i-invest. Huwag hayaang kainin ng lifestyle creep ang extra income.

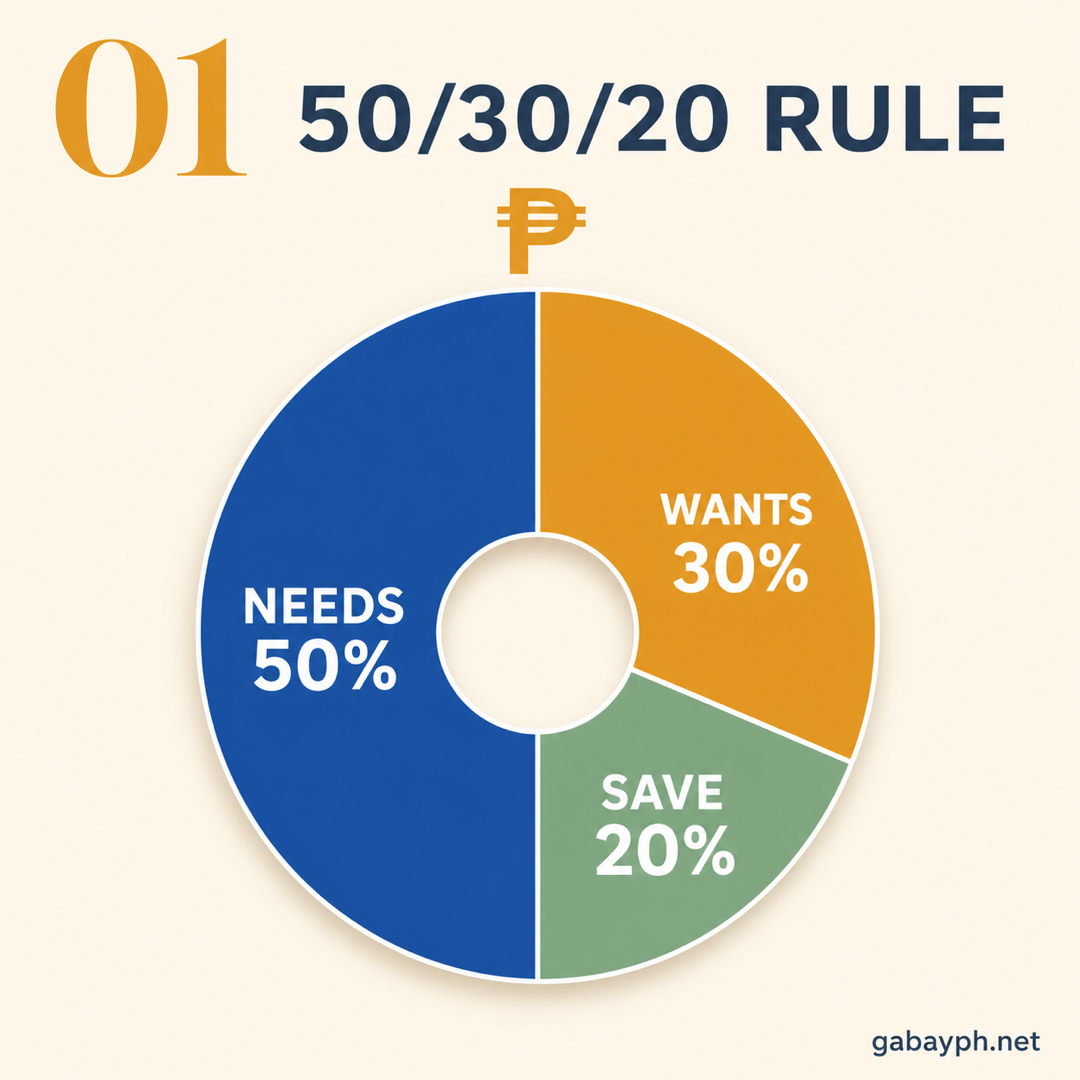

The Filipino 50/30/20 Rule (Adapted for Reality)

Ang Filipino 50/30/20 Rule (Na-adjust para sa Realidad)

You've probably heard of the 50/30/20 rule — the popular budgeting framework where 50% goes to needs, 30% to wants, and 20% to savings. It's a great starting point, pero sa Pilipinas, hindi laging realistic ang exact percentages. Let's adapt it:

50% — Needs (Mga Pangangailangan)

These are non-negotiable expenses. Kung hindi mo babayaran, may problema ka:

- Pagkain — Bigas, ulam, groceries (this alone can eat 30-40% for low-income families)

- Bahay — Rent, amortization, or maintenance

- Kuryente at tubig — Meralco, local water district

- Pamasahe — Daily commute to work and school

- Health — Medicine, check-ups, PhilHealth contributions

30% — Wants (Mga Gusto)

These make life enjoyable pero kaya mong mabuhay nang wala ito:

- Mobile load and data — Promo subscriptions, extra data

- Entertainment — Netflix, Spotify, gaming, tambay budget

- Shopping — Clothes, gadgets, online orders

- Dining out — Jollibee, Mang Inasal, samgyup, milk tea

20% — Savings and Debt Payments (Ipon at Bayad-Utang)

This is your future self thanking you:

- Emergency fund — Target: 3-6 months of expenses

- Pag-IBIG MP2 — Tax-free savings with great returns

- Investments — Stocks, mutual funds, UITFs

- Debt payments — Credit card, loan, or 5-6 payoff (prioritize this!)

The Reality Adjustment

For many Filipino families, especially those earning below ₱25,000/month, needs may take up 70% or more of income. That's okay — don't feel bad about it. The goal is to reduce the needs percentage over time by finding savings (cheaper groceries, lower bills) and protect at least 10% for savings, kahit 5% lang muna. Even ₱500/month na ipon is better than zero.

A more realistic Filipino split might be: 70% needs / 20% wants / 10% savings. Work toward the ideal 50/30/20 as your income grows.

Siguradong narinig mo na ang 50/30/20 rule — ang popular na budgeting framework kung saan 50% ang napupunta sa needs, 30% sa wants, at 20% sa savings. Magandang starting point ito, pero sa Pilipinas, hindi laging realistic ang exact percentages. I-adapt natin ito:

50% — Needs (Mga Pangangailangan)

Ito ang mga non-negotiable na gastos. Kung hindi mo babayaran, may problema ka:

- Pagkain — Bigas, ulam, groceries (ito lang pwedeng kumain ng 30-40% para sa low-income families)

- Bahay — Renta, amortization, o maintenance

- Kuryente at tubig — Meralco, local water district

- Pamasahe — Pang-araw-araw na commute sa trabaho at eskwela

- Kalusugan — Gamot, check-ups, PhilHealth contributions

30% — Wants (Mga Gusto)

Ito ang nagpapasaya ng buhay pero kaya mong mabuhay nang wala ito:

- Mobile load at data — Promo subscriptions, extra data

- Entertainment — Netflix, Spotify, gaming, tambay budget

- Shopping — Damit, gadgets, online orders

- Kain sa labas — Jollibee, Mang Inasal, samgyup, milk tea

20% — Savings at Bayad-Utang (Ipon at Debt Payments)

Ito ang pasasalamatan ng future self mo:

- Emergency fund — Target: 3-6 na buwan na halaga ng gastos

- Pag-IBIG MP2 — Tax-free savings na may magandang returns

- Investments — Stocks, mutual funds, UITFs

- Bayad sa utang — Credit card, loan, o 5-6 payoff (unahin ito!)

Ang Reality Adjustment

Para sa maraming pamilyang Pilipino, lalo na ang kumikita ng below ₱25,000/buwan, ang needs ay pwedeng kumain ng 70% o higit pa ng kita. Okay lang iyon — huwag kang ma-guilty. Ang goal ay bawasan ang needs percentage over time sa pamamagitan ng paghahanap ng matitipid (mas murang groceries, mas mababang bills) at protektahan kahit 10% para sa ipon, kahit 5% lang muna. Kahit ₱500/buwan na ipon ay mas maganda kaysa sa wala.

Ang mas realistic na Filipino split: 70% needs / 20% wants / 10% savings. Magtrabaho patungo sa ideal na 50/30/20 habang lumalaki ang kita mo.

Tracking Your Expenses

Pag-track ng mga Gastos Mo

You can't control what you don't measure. Ang una mong gagawin is i-track kung saan talaga napupunta ang pera mo. Maraming ways to do this — choose the one you'll actually stick to:

Method 1: The Notebook (Papel at Bolpen)

The classic Filipino budgeting method. Get a small notebook dedicated only to expenses. Every day, write down everything you spend — kahit ₱8 na barya sa tubig. Divide the page into columns: Date, Item, Amount, Category. At the end of the week, add everything up. Simple, reliable, at walang kailangan na internet.

Method 2: Phone Notes or Notepad App

If mas lagi kang may phone, use your built-in Notes app. Create a new note each month. List your expenses as you go — quick type lang, no special format needed. Some people like to send themselves a text message or Viber message every time they spend, then total everything at week's end.

Method 3: GCash Transaction History

If you use GCash for most transactions, you already have a built-in expense tracker! Go to GCash > Transaction History to see all your spending. The downside: hindi kasama ang cash expenses mo dito. But if 70%+ of your spending goes through GCash, it's a great start. You can supplement with a small notebook for cash transactions.

Method 4: Spreadsheet (Google Sheets or Excel)

For the more organized, create a simple spreadsheet with columns for Date, Description, Amount, and Category. Google Sheets is free and accessible from any device. You can set up simple formulas to auto-total each category. This method gives you the clearest picture of where money goes, pero it requires more effort.

Tip: Whichever method you choose, do a weekly review every Sunday. Tingnan mo kung on-track ka pa sa budget mo. It only takes 10-15 minutes, and it's the single most important habit for staying on budget.

Hindi mo ma-control ang hindi mo sinusukat. Ang una mong gagawin ay i-track kung saan talaga napupunta ang pera mo. Maraming paraan para gawin ito — piliin ang isa na talagang gagawin mo nang consistent:

Paraan 1: Ang Notebook (Papel at Bolpen)

Ang klasikong Filipino budgeting method. Kumuha ng maliit na notebook na para lang sa gastos. Araw-araw, isulat ang lahat ng ginastos mo — kahit ₱8 na barya sa tubig. Hatiin ang pahina sa mga column: Petsa, Bagay, Halaga, Kategorya. Sa dulo ng linggo, i-total ang lahat. Simple, reliable, at walang kailangan na internet.

Paraan 2: Phone Notes o Notepad App

Kung mas lagi kang may phone, gamitin ang built-in Notes app mo. Gumawa ng bagong note bawat buwan. Ilista ang mga gastos mo habang gumagastos — mabilis na pag-type lang, walang kailangan na special format. Ang iba ay nagpapadala sa sarili nila ng text o Viber message tuwing gumagastos, tapos tino-total lahat sa dulo ng linggo.

Paraan 3: GCash Transaction History

Kung ginagamit mo ang GCash para sa karamihan ng transactions, mayroon ka nang built-in expense tracker! Pumunta sa GCash > Transaction History para makita ang lahat ng gastos mo. Ang downside: hindi kasama ang cash expenses mo dito. Pero kung 70%+ ng spending mo ay dumadaan sa GCash, magandang simula na iyon. Pwede mong dagdagan ng maliit na notebook para sa cash transactions.

Paraan 4: Spreadsheet (Google Sheets o Excel)

Para sa mas organized, gumawa ng simpleng spreadsheet na may columns para sa Petsa, Paglalarawan, Halaga, at Kategorya. Libre ang Google Sheets at accessible mula sa kahit anong device. Pwede kang mag-set up ng simpleng formulas para auto-total ang bawat kategorya. Pinaka-malinaw itong paraan para makita kung saan napupunta ang pera, pero mas madaming effort ang kailangan.

Tip: Kahit anong paraan ang piliin mo, mag-weekly review tuwing Linggo. Tingnan mo kung on-track ka pa sa budget mo. 10-15 minuto lang ang kailangan, at ito ang pinaka-importanteng habit para manatili sa budget.

Try our free tool: Expense Tracker — categorize your income and expenses, see visual breakdowns, and track your budget right in your browser.

Subukan ang aming libreng tool: Expense Tracker — i-categorize ang kita at gastos mo, makita ang visual breakdowns, at i-track ang budget mo mismo sa browser mo.

Palengke vs Supermarket: Where to Save on Groceries

Palengke vs Supermarket: Saan Makakatipid sa Groceries

Food is the biggest expense for most Filipino families — often 30-40% of the budget. The key rule: buy meat, fish, and vegetables at the palengke (20-30% cheaper than supermarket) and buy bulk instead of tingi for non-perishables. Use our Palengke Price Compare tool to check prices, and see our full Cut Monthly Expenses guide for detailed palengke vs supermarket strategies.

Ang pagkain ang pinakamalaking gastos para sa karamihan ng pamilyang Pilipino — madalas 30-40% ng budget. Ang susi: bumili ng karne, isda, at gulay sa palengke (20-30% mas mura kaysa supermarket) at bumili nang bulk imbes na tingi para sa non-perishables. Gamitin ang aming Palengke Price Compare tool para i-check ang presyo, at tingnan ang buong gabay sa Pagbawas ng Buwanang Gastos para sa detalyadong palengke vs supermarket strategies.

Cutting Monthly Costs

Pagbawas ng Buwanang Gastos

Small savings on recurring expenses add up fast. Top quick wins: switch to LED bulbs, unplug appliances on standby, downgrade your internet plan, cancel unused subscriptions, and switch postpaid to prepaid. For detailed strategies on utilities, transport, shopping, and subscriptions, see our Cut Monthly Expenses guide. Track your progress with our Expense Tracker tool.

Ang maliliit na tipid sa recurring expenses ay mabilis dumami. Pinakamabilisang panalo: lumipat sa LED bulbs, i-unplug ang mga appliance sa standby, i-downgrade ang internet plan, i-cancel ang hindi ginagamit na subscriptions, at lumipat sa prepaid mula postpaid. Para sa detalyadong strategies sa utilities, transpo, shopping, at subscriptions, tingnan ang aming gabay sa Pagbawas ng Buwanang Gastos. I-track ang progreso mo gamit ang aming Expense Tracker tool.

Managing Utang and Paluwagan

Pag-manage ng Utang at Paluwagan

Managing utang is a critical part of budgeting. Here are the common debt situations:

The 5-6 System (Bumbay Lending)

Borrow ₱5,000, pay back ₱6,000 — that's 20% interest per month (240%/year). If you're in a 5-6 cycle, breaking free should be your #1 budget priority. Build an emergency fund so you won't need 5-6 next time.

Paluwagan: When It Helps vs When It Hurts

What it is: A group savings system where, say, 10 people each contribute ₱1,000/month. Each month, one person gets the whole pot (₱10,000). It rotates until everyone has had a turn.

When it helps:

- It's a forced savings mechanism — napipilitan kang mag-ipon kasi may commitment ka sa grupo

- No interest charged — unlike loans

- Good for saving toward a specific goal (tuition, appliance, etc.)

When it hurts:

- If someone in the group defaults — you lose money and may not get your turn

- If you get an early draw and spend it on wants instead of needs — you still have to pay the remaining months with nothing to show for it

- No consumer protection — it's all based on trust

Tip: Only join paluwagan with people you deeply trust. Set clear rules upfront. Better yet, use it alongside your own savings — hindi siya replacement for a real emergency fund.

Smarter Debt Alternatives

- SSS Salary Loan — If you're an SSS member, you can borrow up to 2 months' salary at 10% interest per year. Way cheaper than 5-6

- Pag-IBIG Multi-Purpose Loan — Similar to SSS, low interest rates for members

- GCredit or Maya Credit — 5% monthly interest, not great pero better than 5-6

- Cooperative loans — If you're a member of a cooperative, they typically offer 1-2% monthly interest

Ang pag-manage ng utang ay kritikal na bahagi ng budgeting. Narito ang mga karaniwang sitwasyon ng utang:

Ang 5-6 System (Bumbay Lending)

Humiram ng ₱5,000, magbayad ng ₱6,000 — iyon ay 20% interest bawat buwan (240%/taon). Kung nasa 5-6 cycle ka, ang pagtakas dito ang dapat #1 budget priority mo. Mag-build ng emergency fund para hindi mo na kailangan ang 5-6 sa susunod.

Paluwagan: Kailan Nakakatulong vs Kailan Nakakasakit

Ano ito: Isang group savings system kung saan, halimbawa, 10 tao ang nagco-contribute ng ₱1,000/buwan. Bawat buwan, isang tao ang kumukuha ng buong pot (₱10,000). Nag-ro-rotate hanggang lahat ay nagkaroon ng turn.

Kailan nakakatulong:

- Forced savings mechanism — napipilitan kang mag-ipon dahil may commitment ka sa grupo

- Walang interest na sinisingil — hindi tulad ng loans

- Magandang paraan para mag-ipon para sa specific goal (tuition, appliance, atbp.)

Kailan nakakasakit:

- Kung may isa sa grupo na mag-default — mawawalan ka ng pera at baka hindi ka makakuha ng turn mo

- Kung maaga kang nakakuha at ginastos sa gusto imbes na kailangan — kailangan mo pa ring magbayad sa natitirang buwan na wala kang mapapakita

- Walang consumer protection — lahat ay based sa trust

Tip: Sumali lang sa paluwagan kasama ang mga taong lubos mong pinagkakatiwalaan. Maglagay ng malinaw na rules sa simula. Mas maganda, gamitin ito kasabay ng sarili mong savings — hindi siya replacement para sa tunay na emergency fund.

Mas Matalinong Alternatibo sa Utang

- SSS Salary Loan — Kung SSS member ka, pwede kang humiram ng hanggang 2 buwang sweldo sa 10% interest bawat taon. Sobrang mura kumpara sa 5-6

- Pag-IBIG Multi-Purpose Loan — Katulad ng SSS, mababang interest rates para sa members

- GCredit o Maya Credit — 5% monthly interest, hindi maganda pero mas mabuti kaysa sa 5-6

- Cooperative loans — Kung miyembro ka ng cooperative, karaniwang 1-2% monthly interest ang ino-offer nila

Saving on a Tight Budget

Pag-iipon Kahit Mahigpit ang Budget

"Wala akong matitira para mag-ipon" — this is the most common excuse, and it's usually not true. Ang secret: treat savings like a bill. Pay yourself first, hindi yung tirang-tira na lang. Here's how to start kahit super tight ang budget:

The ₱50/Day Challenge

Set aside ₱50 every day. That's roughly one tricycle ride or one street food snack. In one month, that's ₱1,500. In one year, that's ₱18,250. Kung kaya mong i-increase to ₱100/day, that's ₱36,500 in a year — enough for a decent emergency fund. Start today, hindi bukas.

The Coin Jar Method

Every night, empty all the coins from your wallet into a jar or container. Huwag mong galawin. At the end of the month, you'll be surprised — usually ₱300-800 ang naipon. After 6 months, deposit it into your savings account. Simple and painless.

GCash Auto-Save

If you use GCash, set up GSave (powered by CIMB Bank). You can enable automatic transfers every payday — even just ₱100 or ₱200 per transfer. The money goes into a savings account that earns interest, and because it's slightly harder to access than your regular GCash wallet, you're less tempted to spend it. Out of sight, out of mind.

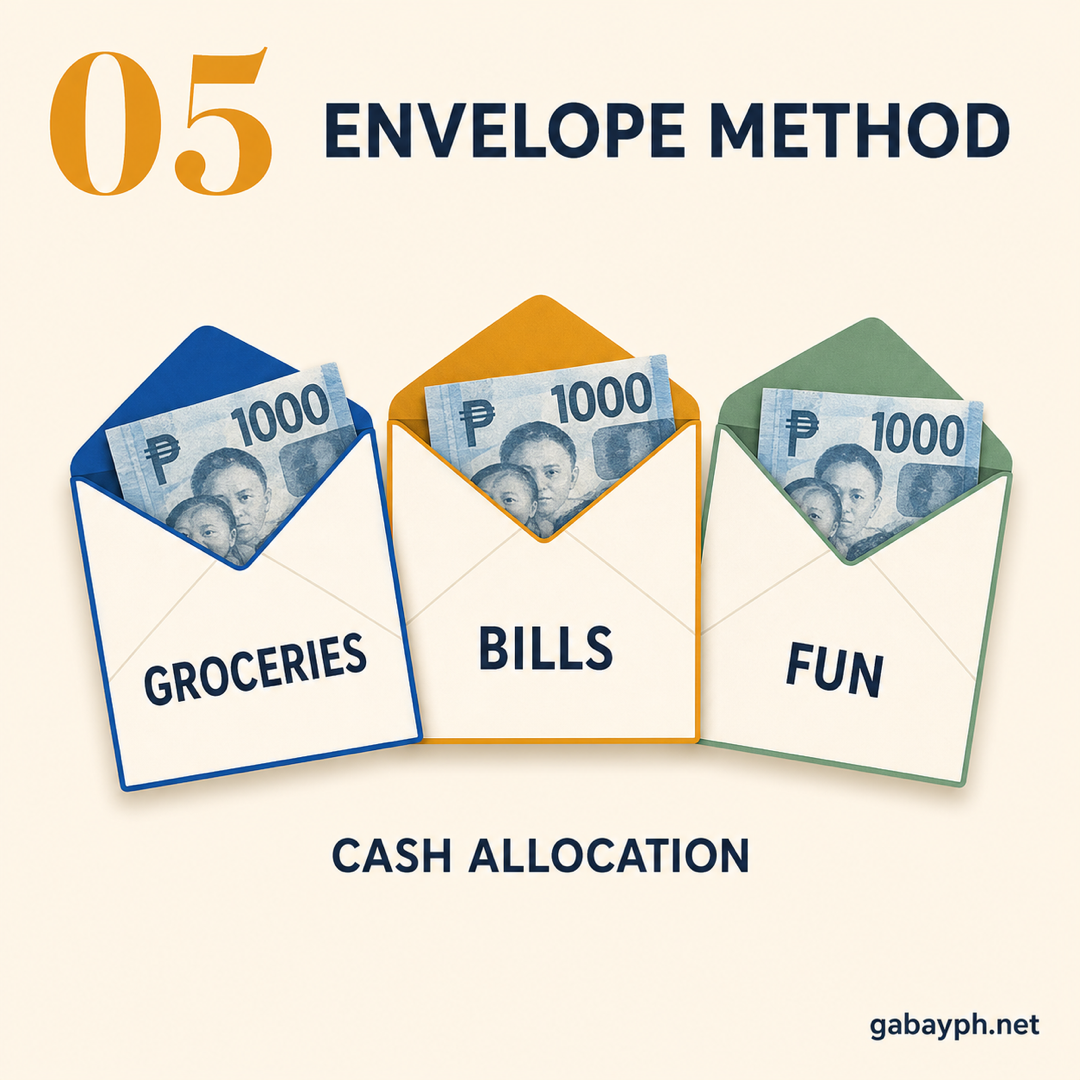

The Envelope Method

Old-school pero effective. Label envelopes for each expense category: Pagkain, Pamasahe, Bills, Ipon, Wants. On payday, put the budgeted cash into each envelope. Once an envelope is empty, stop spending in that category. Ang nandoon sa Ipon envelope — huwag galawin, diretso sa bangko.

Round-Up Savings

Every time you spend, round up the amount and save the difference. Bumili ka ng ulam worth ₱87? Record it as ₱100 and set aside the ₱13 difference. These tiny amounts accumulate surprisingly fast.

"Wala akong matitira para mag-ipon" — ito ang pinakakaraniwang excuse, at karaniwang hindi totoo. Ang secret: tratuhin ang ipon bilang isang bill. Bayaran mo muna ang sarili mo, hindi yung tirang-tira na lang. Narito kung paano magsimula kahit super higpit ang budget:

Ang ₱50/Araw na Challenge

Mag-set aside ng ₱50 araw-araw. Katumbas lang iyan ng isang tricycle ride o isang street food snack. Sa isang buwan, ₱1,500 na iyan. Sa isang taon, ₱18,250. Kung kaya mong i-increase sa ₱100/araw, ₱36,500 iyan sa isang taon — sapat na para sa disenteng emergency fund. Simulan ngayon, hindi bukas.

Ang Coin Jar Method

Gabi-gabi, ilabas lahat ng barya mula sa wallet mo at ilagay sa isang garapon o lalagyan. Huwag mong galawin. Sa dulo ng buwan, magugulat ka — usually ₱300-800 ang naipon. Pagkatapos ng 6 buwan, i-deposit sa savings account mo. Simple at walang sakit.

GCash Auto-Save

Kung gumagamit ka ng GCash, mag-set up ng GSave (powered by CIMB Bank). Pwede mong i-enable ang automatic transfers tuwing payday — kahit ₱100 o ₱200 lang bawat transfer. Napupunta ang pera sa savings account na kumikita ng interest, at dahil medyo mas mahirap i-access kaysa sa regular GCash wallet mo, mas hindi ka na-te-tempt na gastusin ito. Out of sight, out of mind.

Ang Envelope Method

Old-school pero effective. Mag-label ng mga sobre para sa bawat kategorya ng gastos: Pagkain, Pamasahe, Bills, Ipon, Gusto. Sa araw ng sweldo, ilagay ang na-budget na cash sa bawat sobre. Kapag wala nang laman ang isang sobre, tumigil na sa paggastos sa kategoryang iyon. Ang nasa Ipon envelope — huwag galawin, diretso sa bangko.

Round-Up Savings

Tuwing gumagastos ka, i-round up ang halaga at i-save ang pagkakaiba. Bumili ka ng ulam na ₱87? I-record bilang ₱100 at i-set aside ang ₱13 na pagkakaiba. Ang mga maliliit na halaga ay nakaka-accumulate nang surprisingly mabilis.

Pro Tips

Mga Payo

- Pay yourself first. The moment your salary comes in, immediately transfer your savings amount before you spend anything else. Kung hintayin mo ang matira, wala talaga matitira.

- Use the 24-hour rule for non-essential purchases. Want something that costs over ₱500? Wait 24 hours before buying. If you still want it the next day, saka ka bumili. Madalas, mawawala ang urge.

- Plan your meals for the week. Meal planning reduces food waste and impulse food spending. Write down what you'll cook each day, make a grocery list based on that, and stick to it.

- Keep a "no-spend day" once a week. Pick one day where you spend ₱0 on anything non-essential. Bring packed lunch, stay in, use what you already have at home.

- Review and adjust your budget every month. Your first budget won't be perfect — that's normal. Track, review, adjust. By month 3, you'll have a budget that actually works for your family.

- Involve the whole family. Budget works best when everyone's on the same page. Talk to your spouse and older kids about financial goals. When everyone understands the "why," it's easier to stick to the plan.

- Bayaran mo muna ang sarili mo. Sa oras na dumating ang sweldo, agad na i-transfer ang savings amount bago ka gumastos ng kahit ano. Kung hihintayin mo ang matira, wala talaga matitira.

- Gamitin ang 24-hour rule para sa non-essential purchases. May gusto kang bilhin na more than ₱500? Maghintay ng 24 oras bago bumili. Kung gusto mo pa rin kinabukasan, saka ka bumili. Madalas, mawawala ang urge.

- Planuhin ang pagkain para sa linggo. Ang meal planning ay nagbabawas ng food waste at impulse food spending. Isulat kung ano ang iluluto mo bawat araw, gumawa ng grocery list batay dito, at sundin ito.

- Magkaroon ng "no-spend day" isang beses sa isang linggo. Pumili ng isang araw na ₱0 ang gastos sa kahit anong hindi essential. Magdala ng baon, manatili sa bahay, gamitin ang nasa bahay na.

- I-review at i-adjust ang budget mo bawat buwan. Hindi magiging perpekto ang unang budget mo — normal lang iyon. I-track, i-review, i-adjust. Sa ika-3 buwan, magkakaroon ka ng budget na talagang gumagana para sa pamilya mo.

- Isali ang buong pamilya. Mas effective ang budget kapag pare-pareho ang nalalaman ng lahat. Kausapin ang asawa at mas malalaking anak tungkol sa financial goals. Kapag naiintindihan ng lahat ang "bakit," mas madaling sundin ang plano.

Frequently Asked Questions

Mga Madalas Itanong

How much should I save each month?

The ideal target is 20% of your income, but any amount is better than nothing. If you earn ₱15,000/month and can only save ₱500, that's still ₱6,000 per year. Start where you can and gradually increase. The most important thing is consistency — ₱500 every month for 12 months is better than ₱6,000 saved once then nothing for the rest of the year. Kahit barya lang, basta regular.

Magkano ang dapat kong i-save bawat buwan?

Ang ideal na target ay 20% ng kita mo, pero kahit anong halaga ay mas maganda kaysa sa wala. Kung kumikita ka ng ₱15,000/buwan at ₱500 lang ang kaya mong i-save, ₱6,000 pa rin iyan bawat taon. Magsimula kung saan kaya at unti-unting dagdagan. Ang pinakamahalaga ay consistency — ₱500 bawat buwan sa 12 buwan ay mas maganda kaysa sa ₱6,000 na na-save minsan tapos wala na sa buong taon. Kahit barya lang, basta regular.

What's the best budgeting app for Filipinos?

There are several good options, pero honestly, the best app is the one you'll actually use. Here are popular choices among Filipinos:

- Google Sheets — Free, flexible, accessible on any device. Create your own template or find free Filipino budget templates online

- Money Manager (Android/iOS) — Simple expense tracker, free version is more than enough

- GCash transaction history — Not an app per se, but if most of your spending goes through GCash, it doubles as a spending tracker

- Pen and paper — Still the most popular "app" in Filipino households. A ₱20 notebook works perfectly

Don't overthink the tool. Ang mahalaga is you actually track your expenses regularly.

Ano ang pinakamagandang budgeting app para sa mga Pilipino?

Maraming magandang options, pero honestly, ang pinaka-magandang app ay yung talagang gagamitin mo. Narito ang mga popular na choices sa mga Pilipino:

- Google Sheets — Libre, flexible, accessible sa kahit anong device. Gumawa ng sariling template o maghanap ng libreng Filipino budget templates online

- Money Manager (Android/iOS) — Simpleng expense tracker, sobra na ang free version

- GCash transaction history — Hindi app per se, pero kung karamihan ng gastos mo ay dumadaan sa GCash, doble siyang spending tracker

- Papel at bolpen — Pinakapopular pa ring "app" sa mga household na Pilipino. Ang ₱20 na notebook ay gumagana nang maayos

Huwag i-overthink ang tool. Ang mahalaga ay talagang i-track mo ang mga gastos mo nang regular.

How do I budget if my income is irregular?

This is common for freelancers, small business owners, and gig workers sa Pilipinas. The approach: budget based on your lowest monthly income over the past 6 months. If your income ranges from ₱12,000-₱25,000, build your budget around ₱12,000. Any amount above that goes straight to savings or paying off debt. During high-income months, resist the urge to spend more — save the excess para pantapal sa mga lean months.

Paano mag-budget kung hindi regular ang kita ko?

Karaniwan ito sa mga freelancers, small business owners, at gig workers sa Pilipinas. Ang approach: mag-budget batay sa pinakamababang buwanang kita mo sa nakaraang 6 na buwan. Kung ang kita mo ay nasa ₱12,000-₱25,000, i-build ang budget mo sa paligid ng ₱12,000. Kahit anong halaga na lampas doon ay diretso sa ipon o pagbabayad ng utang. Sa mga high-income months, pigilan ang urge na gumastos nang mas malaki — i-save ang sobra para pantapal sa mga lean months.

Should I stop all "wants" spending to save money?

No. A budget that's too strict will fail. You'll burn out and eventually overspend out of frustration. The goal is balance. Allocate a small "fun money" amount — even ₱500-1,000/month for things that make you happy. Basta within budget. Think of it as a sustainability measure: a budget you can stick to for years is better than a "perfect" budget you abandon after 2 weeks. Kailangan din naman natin ng konting kasiyahan.

Dapat bang ihinto ko lahat ng "wants" spending para makatipid?

Hindi. Ang budget na sobrang higpit ay mag-fa-fail. Ma-bu-burn out ka at eventually mag-overspend dahil sa frustration. Ang goal ay balanse. Mag-allocate ng maliit na "fun money" — kahit ₱500-1,000/buwan para sa mga bagay na nagpapasaya sa iyo. Basta within budget. Isipin mo itong sustainability measure: mas maganda ang budget na kaya mong sundin nang matagal kaysa sa "perfect" na budget na tinigilan mo pagkatapos ng 2 linggo. Kailangan din naman natin ng konting kasiyahan.

How do I handle gastos for fiestas, birthdays, and family events?

Filipino culture is celebration-heavy, and these events can wreck a budget if you're not prepared. The solution: create a "celebrations" fund. Set aside ₱500-1,000 per month specifically for upcoming events. Since you usually know when birthdays and fiestas happen, plan ahead. You don't have to be the biggest contributor at every handaan — a modest dish or small regalo is enough. Ang mahalaga ay nandoon ka, hindi kung gaano kalaki ang ambag. Set boundaries respectfully, and don't go into debt for a party.

Paano i-handle ang gastos para sa fiestas, birthdays, at family events?

Ang kulturang Pilipino ay puno ng celebrations, at ang mga events na ito ay pwedeng makasira ng budget kung hindi ka handa. Ang solusyon: gumawa ng "celebrations" fund. Mag-set aside ng ₱500-1,000 bawat buwan para sa mga paparating na events. Dahil karaniwang alam mo kung kailan ang mga birthdays at fiestas, mag-plan ahead. Hindi kailangan na ikaw ang pinaka-malaking ambag sa bawat handaan — isang modest na ulam o maliit na regalo ay sapat na. Ang mahalaga ay nandoon ka, hindi kung gaano kalaki ang ambag. Mag-set ng boundaries nang magalang, at huwag mag-utang para sa party.