Extrajudicial Settlement & Estate Tax: Inheriting Property in the Philippines (2026)

Extrajudicial Settlement at Estate Tax: Pagmana ng Ari-arian sa Pilipinas (2026)

The 5-Step Walkthrough

Extrajudicial settlement in five steps.

Quick Summary

Mabilis na Buod

Legal & Financial Disclaimer

This guide is for informational purposes only and is not legal or tax advice. Estate law and tax rules are complex and fact-specific. Consult a licensed attorney or CPA for your specific situation — especially when real property, multiple heirs, or contested ownership are involved. Tax laws, amnesty deadlines, and BIR rules can change without notice. Verify the latest rules at bir.gov.ph before filing. GabayPH is not a law firm or tax consultancy.

Legal at Financial Disclaimer

Ang gabay na ito ay pang-impormasyon lamang at hindi legal o tax advice. Komplikado ang estate law at tax rules, at depende sa katayuan ng bawat kaso. Kumunsulta sa lisensyadong abogado o CPA para sa inyong sitwasyon — lalo na kung may real property, maraming heir, o may away sa ownership. Maaaring magbago ang tax laws, amnesty deadlines, at BIR rules nang walang abiso. I-verify sa bir.gov.ph bago mag-file. Ang GabayPH ay hindi law firm o tax consultancy.

Table of Contents

Talaan ng Nilalaman

When Extrajudicial Settlement (EJS) is Allowed

Kailan Pwede ang Extrajudicial Settlement (EJS)

Under Rule 74 of the Rules of Court, heirs can settle the estate themselves (no court petition) when ALL of these are true:

Sa ilalim ng Rule 74 ng Rules of Court, pwedeng mismong ayusin ng heirs ang estate (walang petition sa korte) kung LAHAT ng ito ay totoo:

- The deceased did not leave a will (if there is a will, probate is required)

- Walang iniwang will ang namatay (kung may will, kailangan ng probate)

- All heirs are of legal age OR minor heirs have a court-appointed guardian representing them

- Lahat ng heirs ay may edad O may court-appointed guardian ang minor heirs

- No outstanding debts against the estate (or heirs agree to assume them)

- Walang utang ang estate (o sasagutin ng heirs)

- All heirs unanimously agree on how the estate will be divided

- Sang-ayon ang lahat ng heirs sa hatian

If any of these fail, you must file a judicial settlement of estate in the RTC.

Kung hindi naabot ang alinman, kailangang mag-file ng judicial settlement sa RTC.

When You Must Go to Court (Judicial Settlement)

Kailan Kailangang Pumunta sa Korte (Judicial Settlement)

EJS is NOT allowed — you must file a judicial settlement petition — when:

HINDI pwede ang EJS — kailangang mag-petition sa korte — kapag:

- The deceased left a will (requires probate, whether testate or holographic)

- May iniwang will ang namatay (kailangan ng probate)

- A minor heir has no court-appointed guardian

- Walang court-appointed guardian ang minor heir

- Heirs dispute the division of property

- May away sa division ang heirs

- An heir is missing or unreachable (e.g., OFW who cannot be contacted or verified)

- Nawawala o hindi makontak ang isang heir (OFW na hindi makontak)

- Outstanding creditor claims are unresolved

- May utang na hindi pa naaayos

Estate Tax: The 6% Flat Rate & Deductions

Estate Tax: 6% at mga Deductions

Under the TRAIN Law (RA 10963, effective January 1, 2018), estate tax is a flat 6% of the net estate. No brackets, no progressive rates.

Sa ilalim ng TRAIN Law (RA 10963, epektibo Enero 1, 2018), ang estate tax ay flat 6% ng net estate. Walang brackets, walang progressive rates.

Allowable Deductions (Huge — Most Small Estates Owe Zero)

Mga Allowable Deduction (Malaki — Karamihan ng Maliit na Estate ay Zero)

- Standard deduction: ₱5,000,000 (flat, no documentation needed)

- Standard deduction: ₱5,000,000 (flat, walang dokumento)

- Family home: up to ₱10,000,000 additional (only one home; cannot exceed actual value)

- Family home: hanggang ₱10,000,000 dagdag (isang home lang; hindi lalampas sa aktwal)

- Medical expenses: up to ₱500,000 incurred within 1 year before death

- Medical expenses: hanggang ₱500,000 sa loob ng 1 taon bago mamatay

- Funeral expenses: up to ₱200,000

- Funeral expenses: hanggang ₱200,000

- Claims against the estate: actual amount with proof

- Utang ng estate: aktwal na halaga na may proof

- Judicial/administrative expenses: actual amount with proof

- Judicial/admin expenses: aktwal na may proof

Practical effect: A family with a ₱8M house (as family home) + ₱1M in savings = net estate before deduction ₱9M. After ₱5,000,000 standard + ₱8M family home (full value) = net taxable estate is zero. Most inherited family homes owe no estate tax.

Praktikal: Pamilyang may ₱8M na bahay (family home) + ₱1M savings = ₱9M bago deduction. Pagkatapos ng ₱5,000,000 standard + ₱8M family home = zero taxable estate. Karamihan ng minanang bahay ay walang estate tax.

Deadline & Penalties

Deadline at Parusa

Estate tax return (BIR Form 1801) must be filed within 1 year from date of death. Commissioner may grant extension up to 30 days in meritorious cases.

Ang estate tax return (BIR Form 1801) ay kailangang i-file sa loob ng 1 taon mula kamatayan. Pwede mag-extend ng hanggang 30 araw sa meritorious cases.

Late filing penalty: 25% surcharge + 12% annual interest from the original deadline. A ₱200K estate tax bill unpaid for 3 years accumulates about ₱272K in interest alone — often more than the tax itself.

Parusa sa late: 25% surcharge + 12% annual interest mula sa orihinal na deadline. Ang ₱200K estate tax na hindi bayad sa loob ng 3 taon ay may ~₱272K interest — higit pa kaysa mismong tax.

Estate Tax Amnesty Status (verify before relying on this)

Estate Tax Amnesty Status (verify muna)

Important timing note: The previous Estate Tax Amnesty under RA 11956 EXPIRED June 14, 2025. As of April 25, 2026, a new extension bill had passed both houses of Congress (House vote 280-0; Senate approved) and was awaiting presidential action. Under the 1987 Constitution, a bill becomes law if the President neither signs nor vetoes it within 30 days. The 30-day window from April 25 has since elapsed — the extension has either been signed or lapsed into law, but the exact status and BIR implementing rules should be confirmed before filing.

The proposed extension would cover decedents who died on or before December 31, 2024 and give heirs until December 31, 2028 to settle. Confirm the law's effectivity and the implementing BIR Revenue Regulation before relying on the amnesty rates — see bir.gov.ph/estate-tax and the Official Gazette for the published act and implementing rules.

Importanteng paalala: Ang dating Estate Tax Amnesty sa ilalim ng RA 11956 ay EXPIRED June 14, 2025. Noong April 25, 2026, may bagong extension bill na ipinasa sa dalawang kapulungan ng Kongreso (House 280-0; Senate approved) at hinihintay ang aksyon ng Pangulo. Sa ilalim ng 1987 Constitution, ang isang bill ay nagiging batas kung hindi pinipirmahan o ni-veto ng Pangulo sa loob ng 30 araw. Lumipas na ang 30-day window mula Abril 25 — pirmado na o naging batas na sa lapse, pero kailangang i-confirm ang eksaktong status at BIR implementing rules bago mag-file.

Saklaw ng panukala ang mga namatay bago o sa December 31, 2024 at bibigyan ang heirs hanggang December 31, 2028 para mag-settle. I-confirm ang effectivity ng batas at ang BIR Revenue Regulation bago umasa sa amnesty rates — tingnan ang bir.gov.ph/estate-tax at ang Official Gazette para sa published act at implementing rules.

Step-by-Step Process

Hakbang-Hakbang na Proseso

-

Gather Documents

You need:

- PSA death certificate (multiple certified copies)

- Original Transfer Certificates of Title (TCTs) for real properties

- Tax declarations from Assessor's Office

- BIR Form 1904 to secure a TIN for the estate

- TINs of all heirs (each heir must have one)

- PSA birth certificates for all heirs

- PSA marriage certificate if spouse is an heir

- Bank statements, stock certificates, vehicle OR/CR for all other estate assets

- Latest real property tax (RPT) clearance from Assessor's Office

-

Prepare & Notarize the Deed of Extrajudicial Settlement

Hire a lawyer to draft the Deed. It must describe each property, list every heir with their respective shares, and include adjudication language. Attorney's fee: ₱25,000-₱100,000 typically, or 1-5% of gross estate. Notarization: ₱1,000-₱5,000 or 0.1-1% of estate value.

-

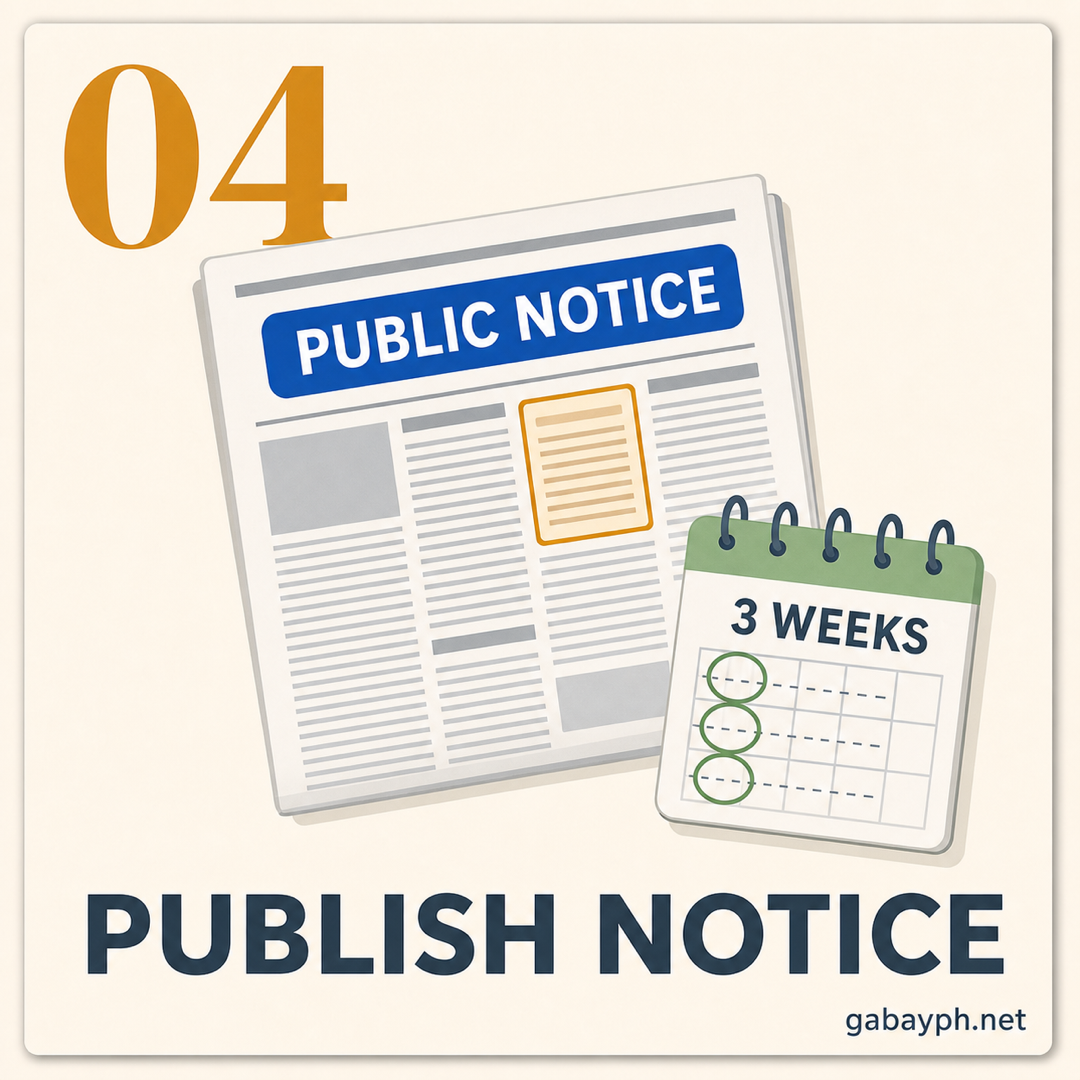

Publish in a Newspaper of General Circulation (MANDATORY)

Publish the notice of the EJS once a week for 3 consecutive weeks (Rule 74 requirement). Not optional, not negotiable — even if all heirs are in the same room. This is statutory notice to unknown creditors.

Cost: ₱6,000-₱12,000 Metro Manila; ₱3,000-₱8,000 in provincial papers. Keep the publisher's affidavit — BIR and Registry of Deeds will ask for it.

Creditors have 2 years from publication to contest the settlement under Rule 74 Sec. 4.

-

File BIR Form 1801 & Pay Estate Tax

File at the BIR Revenue District Office (RDO) where the decedent was domiciled at time of death. Pay via Authorized Agent Bank (AAB) or eFPS.

Documents to submit: death certificate, notarized Deed of EJS, publisher's affidavit, copies of titles, tax declarations, zonal valuations (from BIR zonal table), estate TIN confirmation, all heirs' TINs, and list of all properties and valuations.

Computation reminder: gross estate − allowable deductions = net estate; net estate × 6% = estate tax due. Include all real properties (houses, lots, condos) AND personal properties (bank accounts, stocks, vehicles).

-

Kunin ang Lahat ng Dokumento

Kailangan mo:

- PSA death certificate (maraming certified copies)

- Orihinal na Transfer Certificate of Title (TCT) ng mga real property

- Tax declarations mula sa Assessor's Office

- BIR Form 1904 para sa TIN ng estate

- TINs ng lahat ng heirs (isa-isa)

- PSA birth certificates ng lahat ng heirs

- PSA marriage certificate kung may asawa

- Bank statements, stock certificates, vehicle OR/CR para sa iba pang assets

- Latest real property tax (RPT) clearance mula Assessor's Office

-

Ipagawa at Pa-notaryohan ang Deed of Extrajudicial Settlement

Kumuha ng abogado para gawin ang Deed. Dapat ito'y detalyado sa bawat property, listahan ng heirs at shares, at may adjudication language. Abogado: ₱25,000-₱100,000, o 1-5% ng gross estate. Notary: ₱1,000-₱5,000.

-

I-publish sa Pahayagan (KAILANGAN)

I-publish ang EJS notice isang beses kada linggo sa loob ng 3 magkakasunod na linggo (Rule 74). Hindi optional — kahit magkakakasama ang lahat ng heirs. Ito ay statutory notice sa mga posibleng creditor.

Bayad: ₱6,000-₱12,000 sa Metro Manila; ₱3,000-₱8,000 sa probinsiyang pahayagan. Itago ang publisher's affidavit — hihingin ito ng BIR at Registry of Deeds.

May 2 taon mula publication ang mga creditor para i-contest (Rule 74 Sec. 4).

-

I-file ang BIR Form 1801 at Magbayad ng Estate Tax

I-file sa BIR RDO ng huling tirahan ng namatay. Magbayad sa Authorized Agent Bank (AAB) o eFPS.

Dokumento: death certificate, notarized Deed of EJS, publisher's affidavit, kopya ng titles, tax declarations, zonal values, estate TIN, TINs ng heirs, at listahan ng lahat ng properties.

Kompyut: gross estate − deductions = net estate; net estate × 6% = estate tax. Isama lahat — real property (bahay, lote, condo) AT personal property (bank account, stocks, sasakyan).

-

Obtain the eCAR (Electronic Certificate Authorizing Registration)

After BIR confirms payment and documents, it issues one eCAR per real property (or bank account). Processing: 5-30 working days at the RDO. Fee: ₱260 per CAR + ₱30 DST per copy. eCAR is valid for 5 years.

The eCAR is the "green light" for Registry of Deeds to cancel the old title and issue a new one. Without it, no title transfer can happen.

-

Pay LGU Transfer Tax

Paid at the City/Municipal Treasurer's Office. Rate: 0.5% in most LGUs; 0.75% in Metro Manila cities (Manila, QC, Makati, etc.). Based on the highest of zonal value, assessed value, or consideration.

-

Register with Registry of Deeds (RoD)

Bring: eCAR, owner's duplicate title, notarized EJS, publisher's affidavit, LGU transfer tax receipt, real property tax clearance. The RoD cancels the old title and issues new title(s) in the heirs' names. Registration fee: approximately 0.25% of property value, sliding scale per LRA schedule. Timeline: 1-4 weeks post-eCAR submission.

-

Update Tax Declaration at Assessor's Office

Bring: new title (post-RoD), Registry of Deeds annotation, EJS. The Assessor cancels the decedent's tax declaration and issues new ones in heirs' names. This is needed for future annual real property tax billing.

Do not skip this step. Many families stop after RoD issuance, then years later find the tax declaration still in the decedent's name — which blocks future sale or mortgage.

-

Kunin ang eCAR (Electronic Certificate Authorizing Registration)

Matapos ma-confirm ng BIR ang bayad at dokumento, iisyu nito ang eCAR — isa bawat real property (o bank account). Proseso: 5-30 working days. Bayad: ₱260 per CAR + ₱30 DST per copy. 5 taon ang bisa ng eCAR.

Ang eCAR ang "green light" para sa Registry of Deeds na mag-issue ng bagong title.

-

Bayaran ang LGU Transfer Tax

Sa City/Municipal Treasurer's Office. Rate: 0.5% karaniwang LGU; 0.75% sa Metro Manila (Manila, QC, Makati, atbp). Base sa pinakamataas ng zonal value, assessed value, o consideration.

-

Mag-register sa Registry of Deeds (RoD)

Dalhin: eCAR, owner's duplicate title, notarized EJS, publisher's affidavit, LGU transfer tax receipt, real property tax clearance. Kanselahin ng RoD ang lumang title at mag-issue ng bago sa pangalan ng heirs. Bayad: ~0.25% ng property value. Tagal: 1-4 linggo.

-

I-update ang Tax Declaration sa Assessor's Office

Dalhin: bagong title, annotation, EJS. I-update ng Assessor ang tax declaration sa pangalan ng heirs. Kailangan ito sa future na annual real property tax.

Huwag laktawan. Maraming pamilya ang humihinto matapos ng RoD, tapos sa ilang taon, tax declaration pa rin sa namatay — hindi na pwedeng ibenta o i-mortgage.

Total Cost Breakdown (Sample: ₱3M Residential Lot in Cavite)

Buong Gastos (Sample: ₱3M na Lote sa Cavite)

Net estate after ₱5,000,000 standard deduction = negative = ₱0 estate tax. But you still pay:

Net estate pagkatapos ng ₱5,000,000 standard deduction = negative = ₱0 estate tax. Pero may bayaran pa rin:

- Attorney's fee: ₱25,000-₱50,000

- Abogado: ₱25,000-₱50,000

- Notarization: ₱2,000-₱5,000

- Notary: ₱2,000-₱5,000

- Newspaper publication (3 weeks): ₱6,000-₱12,000

- Newspaper publication: ₱6,000-₱12,000

- BIR eCAR: ₱260 + ₱30 DST

- BIR eCAR: ₱260 + ₱30 DST

- LGU transfer tax (0.5% of ₱3M): ₱15,000

- LGU transfer tax (0.5% ng ₱3M): ₱15,000

- Registry of Deeds (≈0.25%): ₱7,500

- Registry of Deeds (~0.25%): ₱7,500

- Miscellaneous (certified copies, travel, IT fees): ₱2,000-₱5,000

- Miscellaneous: ₱2,000-₱5,000

Total typical cash outlay: ₱55,000-₱95,000 — even when there's no estate tax at all.

Karaniwang gastos: ₱55,000-₱95,000 — kahit walang estate tax.

Common Traps & Mistakes

Madalas na Pagkakamali

- Skipping or shortcutting the publication. Not three separate calendar weeks = legally defective EJS. Creditors can void it within 2 years.

- Kinakaltas o pinaiikli ang publication. Kung hindi tatlong hiwalay na linggo — may depekto. Pwedeng i-void ng creditors sa loob ng 2 taon.

- Omitting an illegitimate child. Illegitimate children are compulsory heirs under the Family Code. Omitting one exposes the estate to a later legitime claim.

- Hindi isinasama ang illegitimate child. Compulsory heir sila sa Family Code. Kung hindi isinama, maaaring habulin sa legitime sa kalaunan.

- Filing late and accumulating penalties. 25% surcharge + 12% annual interest stacks fast. File within 1 year even if you're still gathering documents — ask BIR for extension rather than filing late.

- Late filing at sumasama ang parusa. 25% + 12% taun-taon. Mag-file sa loob ng 1 taon — humingi ng extension sa BIR kaysa mag-late.

- Stopping at eCAR and never transferring the title. The finish line is RoD + Assessor's Office update. eCAR alone doesn't move the title.

- Huminto sa eCAR at hindi natuloy ang title transfer. Ang finish line ay RoD + Assessor update. Ang eCAR lang ay hindi sapat.

- Having a minor heir without a guardian. Requires a court-appointed guardian before EJS. Absent that, judicial settlement is mandatory.

- Minor heir na walang guardian. Kailangan ng court-appointed guardian bago EJS. Kung wala, judicial settlement ang daan.

- Failing to notify a known creditor. A creditor not a party to the EJS can pursue the claim within 2 years of publication — they don't have to wait until after the title transfers.

- Hindi ibinabalita sa known creditor. Pwede silang habulin sa loob ng 2 taon mula publication.

Pro Tips

Mga Payo

- The standard deduction of ₱5,000,000 kills estate tax on most family homes. Before paying a lawyer to "compute" estate tax, add up your gross estate. If it's under ₱5,000,000 (or under ₱15M including the family home deduction), your tax bill is zero — but you still need the full EJS process for title transfer.

- Ang ₱5,000,000 standard deduction ang nakakapawi ng estate tax sa karamihan ng family home. Bago bayaran ang abogado, i-total ang gross estate. Kung under ₱5,000,000 (o ₱15M kasama ang family home), zero ang tax — pero kailangan pa rin ng buong EJS process.

- Get multiple certified copies of the PSA death certificate upfront. You'll need at least 5-8 copies for BIR, RoD, Assessor, bank accounts, and safekeeping. Each costs ~₱155.

- Kumuha ng maraming PSA death certificate agad. Kailangan ng 5-8 kopya para sa BIR, RoD, Assessor, bank accounts, at reserve. ~₱155 bawat isa.

- Check BIR zonal values before computing. BIR uses zonal value OR assessed value OR actual consideration, WHICHEVER IS HIGHER. Zonal values are at bir.gov.ph and often higher than what's on the tax declaration. Underestimating the property value = BIR assessment letter and penalties.

- I-check ang BIR zonal values bago kompyutin. Ang BIR ay gumagamit ng zonal O assessed O actual, ALIN ANG PINAKAMATAAS. Madalas mas mataas ang zonal. Kung minimal ang sinabing halaga — magpapadala ang BIR ng assessment at parusa.

- Keep the publisher's affidavit in multiple places. You'll reference it at BIR and RoD. Losing it costs weeks of re-publishing in some cases.

- Maraming kopya ng publisher's affidavit. Hihingin sa BIR at RoD. Kung nawala, pwedeng linggo ng re-publishing.

- Consider the 2-year creditor window before major decisions. Heirs sometimes sell inherited property immediately after title transfer — but a creditor's claim can surface during that 2-year window and trigger refund demands or litigation.

- Isaalang-alang ang 2-year creditor window bago mga desisyon. Minsan naibebenta agad ng heirs ang minanang property, pero maaari pang lumabas ang creditor sa loob ng 2 taon at humingi ng refund o litigation.

- If amnesty is revived, move fast. Past amnesties were extended multiple times, but each iteration had cutoff dates. If the new extension passes in 2026, file as early as possible rather than wait — extensions are not guaranteed.

- Kung na-revive ang amnesty, mabilisan. Ang mga nakaraang amnesty ay na-extend pero may cutoff. Kung papasa ang bagong extension sa 2026, mag-file agad kaysa maghintay — hindi garantisado ang extension.

Frequently Asked Questions

Mga Madalas Itanong

How long does the full EJS process take?

Minimum 2-4 months end-to-end: document gathering 1-2 weeks + publication 3 weeks + BIR processing 2-8 weeks + RoD registration 1-4 weeks. Contested cases or incomplete documents stretch this significantly.

Gaano katagal ang buong EJS process?

Minimum 2-4 buwan: dokumento 1-2 linggo + publication 3 linggo + BIR 2-8 linggo + RoD 1-4 linggo. Kung may dispute o kulang sa docs, mas matagal pa.

Can I do EJS without a lawyer?

Legally, yes — the law doesn't require counsel. Practically, no — drafting the Deed correctly, dealing with BIR assessments, and handling RoD issues need legal expertise. The cost of getting it wrong (re-litigation, voided settlement) dwarfs attorney's fees.

Pwede bang mag-EJS na walang abogado?

Legally oo — hindi iniaatas ng batas. Sa totoong buhay, hindi — ang pagdrafting ng Deed, pag-aasikaso ng BIR, at RoD ay nangangailangan ng legal expertise. Ang gastos ng pagkakamali ay mas mahal kaysa fee ng abogado.

What if one heir refuses to sign?

EJS requires unanimous consent. If any heir refuses, you cannot use EJS — you must file a judicial settlement petition at the RTC. The court will adjudicate.

Paano kung may heir na hindi pumipirma?

Kailangan ng unanimous consent sa EJS. Kung may tumatanggi, hindi pwede ang EJS — kailangang mag-file ng judicial settlement sa RTC. Hahatulan ito ng korte.

Does EJS handle bank accounts and vehicles too?

Yes. Any asset the decedent owned — bank accounts, stocks, vehicles — is part of the estate and can be covered in the EJS. Each may need its own release process with the respective institution (bank, PSE, LTO) after the estate is settled.

Saklaw ba ng EJS ang bank accounts at sasakyan?

Oo. Anumang asset ng namatay — bank account, stocks, sasakyan — ay bahagi ng estate. Bawat isa ay may sariling release process sa respective institution matapos ng settlement.

Is the family home deduction available to everyone?

The family home deduction (up to ₱10,000,000) applies if the decedent actually resided in that home with the family at time of death. It cannot exceed the home's actual value. Documentation (voter's certification, utility bills in decedent's name, barangay certification) may be required.

Available ba ang family home deduction sa lahat?

Ang family home deduction (hanggang ₱10M) ay applicable kung talagang tinitirhan ng namatay ang bahay kasama ang pamilya sa oras ng kamatayan. Hindi lalampas sa aktwal na halaga. Maaaring hingin ang voter's cert, utility bills, barangay cert.