SSS, PhilHealth, and Pag-IBIG for Informal Workers (2026 Guide)

SSS, PhilHealth, at Pag-IBIG para sa mga Informal Workers (2026 Gabay)

5 Things to Know

Informal worker benefits in five facts.

Quick Summary

Mabilis na Buod

Table of Contents

Talaan ng Nilalaman

Kaya Mo Ba? (Can You Afford It?)

Kaya Mo Ba?

Let's be honest. If you earn P300-500 a day washing clothes, selling fish at the palengke, or driving a tricycle, paying P1,450 a month for government benefits feels impossible. That's 3 to 5 days of your income just for contributions. We hear you.

Maging totoo tayo. Kung P300-500 lang ang kinikita mo sa isang araw sa paglalaba, pagtitinda ng isda sa palengke, o pagda-drive ng tricycle, parang imposible ang P1,450 bawat buwan para sa government benefits. Iyan ay 3 hanggang 5 araw ng iyong kita para lang sa contributions. Naiintindihan namin.

But here's the reality: one hospital stay without PhilHealth can cost you P50,000-P200,000 — wiping out years of savings or putting your family in debt. The question isn't whether you can afford to pay. It's whether you can afford not to.

Pero ito ang realidad: isang pag-confine sa ospital nang walang PhilHealth ay maaaring P50,000-P200,000 — mawawala ang ipon ng maraming taon o mababaon sa utang ang pamilya mo. Ang tanong ay hindi kung kaya mong magbayad. Ang tanong ay kaya mo bang hindi magbayad.

The good news: you don't have to pay all three at once. Start with what you can afford and build up over time. Here's our recommended priority order:

Ang magandang balita: hindi mo kailangang bayaran ang tatlo nang sabay. Magsimula sa kaya mo at dagdagan habang tumatagal. Ito ang inirerekomenda naming pagkakasunud-sunod:

- PhilHealth first (₱500/month) — Hospital coverage that can save you hundreds of thousands in a single emergency. This is your most important safety net.

- SSS second (₱750/month minimum) — Builds toward retirement pension, gives access to salary loans, sickness and maternity benefits.

- Pag-IBIG third (₱200/month) — Cheapest of the three. Unlocks multi-purpose loans after 24 months and the high-yield MP2 savings program.

- PhilHealth muna (₱500/buwan) — Hospital coverage na maaaring makatipid ng daan-daang libo sa isang emergency. Ito ang pinaka-importanteng safety net mo.

- SSS pangalawa (₱750/buwan minimum) — Nagti-build toward retirement pension, nagbibigay ng access sa salary loans, sickness at maternity benefits.

- Pag-IBIG pangatlo (₱200/buwan) — Pinakamura sa tatlo. Nag-u-unlock ng multi-purpose loans pagkatapos ng 24 months at ng high-yield MP2 savings program.

If ₱500/month for PhilHealth is all you can manage right now, that's already a huge step. You can add SSS and Pag-IBIG when your income allows.

Kung ₱500/buwan para sa PhilHealth lang ang kaya mo ngayon, malaking hakbang na iyon. Maaari mong idagdag ang SSS at Pag-IBIG kapag pumayag na ang kita mo.

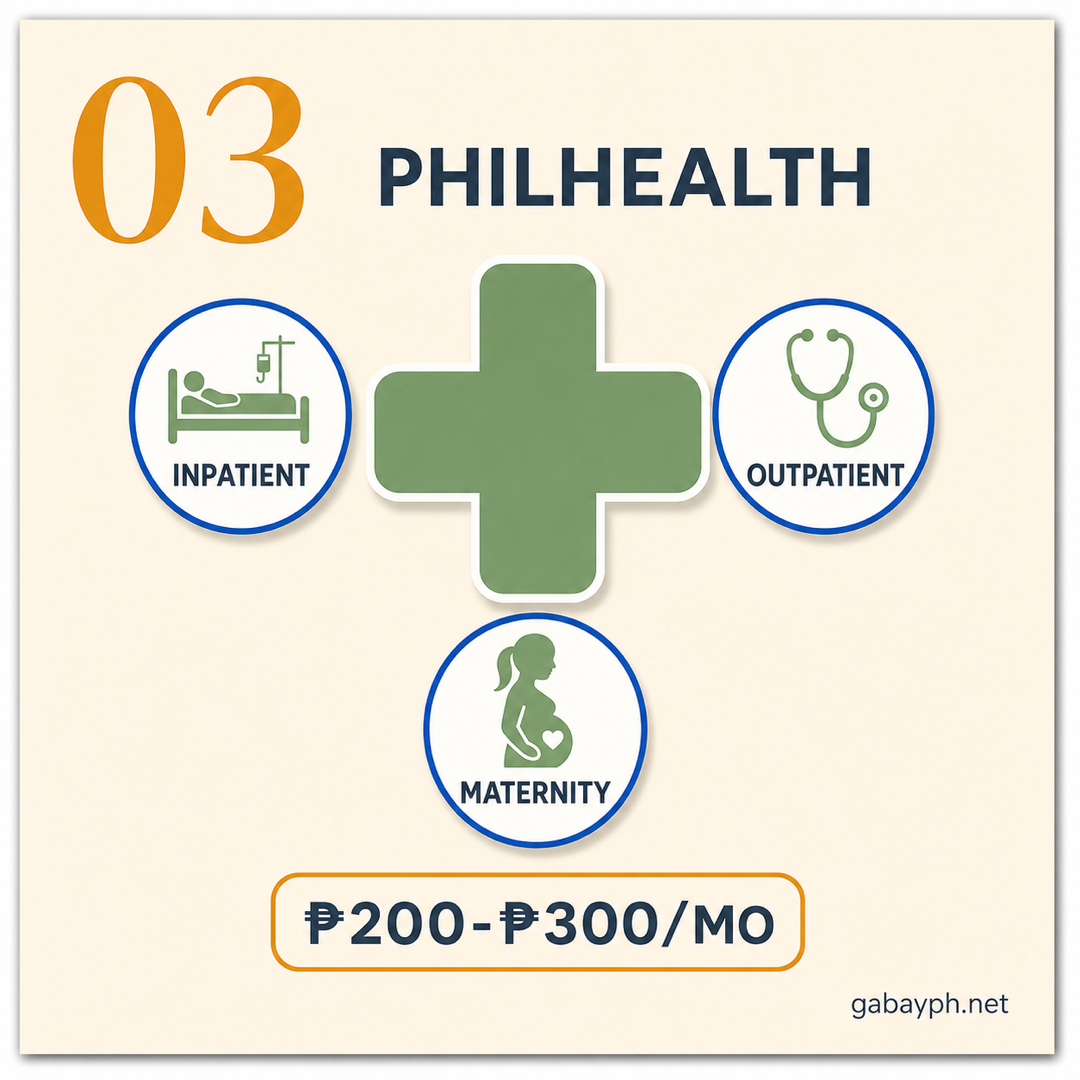

Priority 1: PhilHealth (₱500/month)

Priority 1: PhilHealth (₱500/buwan)

PhilHealth is non-negotiable for informal workers. A single hospital admission can cost more than your entire year's income. PhilHealth's Informal Economy (IE) membership gives you and your dependents access to the same hospital coverage as formal employees.

Ang PhilHealth ay hindi pwedeng wala para sa informal workers. Isang hospital admission lang ay maaaring higit pa sa buong kita mo sa isang taon. Ang Informal Economy (IE) membership ng PhilHealth ay nagbibigay sa iyo at sa mga dependents mo ng parehong hospital coverage gaya ng mga empleyado.

How to Register

Paano Mag-register

- Go to your nearest PhilHealth Local Health Insurance Office (LHIO)

- Fill out the PhilHealth Member Registration Form (PMRF)

- Bring one valid ID (even barangay ID works)

- Select "Informal Economy" as your membership category

- You'll receive your PhilHealth Identification Number (PIN) on the spot

- Pumunta sa pinakamalapit na PhilHealth Local Health Insurance Office (LHIO)

- Punan ang PhilHealth Member Registration Form (PMRF)

- Magdala ng isang valid ID (kahit barangay ID ay tinatanggap)

- Piliin ang "Informal Economy" bilang membership category mo

- Matatanggap mo ang PhilHealth Identification Number (PIN) mo agad-agad

Payment Options

Mga Opsyon sa Pagbabayad

You don't have to pay monthly. PhilHealth allows IE members to pay in larger chunks, which can be easier to budget for:

Hindi mo kailangang magbayad buwan-buwan. Pinapayagan ng PhilHealth ang IE members na magbayad nang mas malaki nang mas madalang, na maaaring mas madaling i-budget:

- Monthly: P500

- Quarterly: P1,500 (every 3 months)

- Semi-annual: P3,000 (every 6 months)

- Annual: P6,000 (once a year)

- Buwanan: P500

- Quarterly: P1,500 (kada 3 buwan)

- Semi-annual: P3,000 (kada 6 na buwan)

- Annual: P6,000 (isang beses sa isang taon)

What PhilHealth Covers

Ano ang Sinasaklaw ng PhilHealth

- Konsulta Package — free consultations and select medicines at accredited health centers. No hospital needed, walang gastos.

- Inpatient coverage — normal delivery up to P9,750, C-section up to P37,050, plus room and board, drugs, labs, and professional fees.

- Z-Benefits — coverage for catastrophic illnesses (certain cancers, kidney transplant, coronary bypass) worth P100,000 to P600,000.

- Outpatient packages — selected procedures like hemodialysis, radiotherapy, and cataract surgery.

- Konsulta Package — libreng konsultasyon at piling gamot sa mga accredited health centers. Hindi kailangan ng ospital, walang gastos.

- Inpatient coverage — normal delivery hanggang P9,750, C-section hanggang P37,050, kasama ang room and board, gamot, labs, at professional fees.

- Z-Benefits — coverage para sa catastrophic illnesses (ilang uri ng cancer, kidney transplant, coronary bypass) na nagkakahalaga ng P100,000 hanggang P600,000.

- Outpatient packages — mga piling procedure tulad ng hemodialysis, radiotherapy, at cataract surgery.

For the full registration and benefits guide, see our complete PhilHealth guide.

Para sa buong registration at benefits guide, tingnan ang aming kumpletong PhilHealth guide.

Priority 2: SSS (₱750/month minimum)

Priority 2: SSS (₱750/buwan minimum)

SSS is your long-term safety net. The minimum voluntary contribution is ₱750/month, which builds toward a retirement pension, gives you access to salary loans, and provides sickness, maternity, and disability benefits. For informal workers, the SSS Voluntary or Self-Employed membership is the right category.

Ang SSS ang long-term safety net mo. Ang minimum voluntary contribution ay ₱750/buwan, na nagbi-build toward retirement pension, nagbibigay ng access sa salary loans, at nagbibigay ng sickness, maternity, at disability benefits. Para sa mga informal workers, ang SSS Voluntary o Self-Employed membership ang tamang category.

How to Register

Paano Mag-register

- Go to the nearest SSS branch or register online at member.sss.gov.ph

- Fill out the SSS Form E-1 (Self-Employed/Voluntary Member Registration)

- Bring one valid ID and proof of date of birth (PSA birth certificate if available)

- You'll receive your SS number immediately after processing

- Create your My.SSS online account to generate Payment Reference Numbers (PRNs) and track contributions

- Pumunta sa pinakamalapit na SSS branch o mag-register online sa member.sss.gov.ph

- Punan ang SSS Form E-1 (Self-Employed/Voluntary Member Registration)

- Magdala ng isang valid ID at proof of date of birth (PSA birth certificate kung mayroon)

- Matatanggap mo ang SS number mo agad pagkatapos ng processing

- Gumawa ng My.SSS online account para maka-generate ng Payment Reference Numbers (PRNs) at ma-track ang contributions

What P750/Month Gets You

Ano ang Makukuha Mo sa P750/Buwan

- Sickness benefit — 90% of your average daily salary credit (ADSC) for up to 120 days per year if you can't work due to illness or injury. Requires at least 3 monthly contributions in the 12 months before your semester of sickness.

- Maternity benefit — 100% of ADSC for 105 days (normal delivery) or 120 days (C-section). Solo parents get an additional 15 days. Requires at least 3 monthly contributions in the 12 months before your semester of delivery.

- Disability benefit — monthly pension if you become permanently disabled. Requires at least 36 months of contributions.

- Retirement pension — monthly pension starting at age 60. Requires at least 120 months (10 years) of contributions. Even P750/month for 10 years gives you a guaranteed monthly pension for life.

- Funeral benefit — ₱20,000–₱60,000 for your beneficiaries, depending on total contributions.

- Salary loan — borrow up to 1 month's salary credit after 36 months of contributions. Interest: 8% per annum, much cheaper than informal "5-6" lending at 20% per month.

- Sickness benefit — 90% ng average daily salary credit (ADSC) mo hanggang 120 araw bawat taon kung hindi ka makapagtrabaho dahil sa sakit o injury. Kailangan ng hindi bababa sa 3 monthly contributions sa 12 buwan bago ang iyong semester ng pagkakasakit.

- Maternity benefit — 100% ng ADSC sa loob ng 105 araw (normal delivery) o 120 araw (C-section). Dagdag 15 araw para sa solo parents. Kailangan ng hindi bababa sa 3 monthly contributions sa 12 buwan bago ang semester ng panganganak.

- Disability benefit — buwanang pension kung ikaw ay permanenteng na-disable. Kailangan ng hindi bababa sa 36 months ng contributions.

- Retirement pension — buwanang pension simula sa edad 60. Kailangan ng hindi bababa sa 120 months (10 taon) ng contributions. Kahit P750/buwan sa loob ng 10 taon, may garantisadong buwanang pension ka habambuhay.

- Funeral benefit — ₱20,000–₱60,000 para sa iyong mga beneficiary, depende sa kabuuang contributions.

- Salary loan — manghiram ng hanggang 1 buwan na salary credit pagkatapos ng 36 months ng contributions. Interest: 8% bawat taon, mas mura kaysa sa "5-6" na 20% bawat buwan.

NEW: SSS Micro Loan Program

BAGO: SSS Micro Loan Program

The SSS Micro Loan Program lets eligible members borrow P1,000 to P20,000 at just 8% annual interest — far cheaper than the "5-6" lending (20% per month) that traps many informal workers in debt cycles. If you need emergency cash, this is the formal alternative that won't bury you.

Ang SSS Micro Loan Program ay nagpapahiram sa mga kwalipikadong miyembro ng P1,000 hanggang P20,000 sa 8% annual interest lang — mas mura kaysa sa "5-6" lending (20% bawat buwan) na nagtatrampa sa maraming informal workers sa debt cycles. Kung kailangan mo ng emergency cash, ito ang formal na alternatibo na hindi ka babaon.

For the full SSS guide, see our complete SSS guide.

Para sa buong SSS guide, tingnan ang aming kumpletong SSS guide.

Priority 3: Pag-IBIG (₱200/month)

Priority 3: Pag-IBIG (₱200/buwan)

Pag-IBIG (HDMF) has the lowest minimum contribution of the three at just ₱200/month. Even if you can't afford SSS or PhilHealth yet, P200 a month is something many informal workers can start with. It's also the easiest to register for.

Ang Pag-IBIG (HDMF) ang may pinakamababang minimum contribution sa tatlo sa ₱200/buwan lang. Kahit hindi mo pa kayang bayaran ang SSS o PhilHealth, ang P200 isang buwan ay kaya ng maraming informal workers na simulan. Ito rin ang pinakamadaling pagpag-register-an.

Benefits You Get

Mga Benepisyong Makukuha Mo

- Multi-Purpose Loan (MPL) — borrow up to 80% of your total savings after 24 months of contributions. Low interest at 10.5% per annum. Payable in up to 24 months.

- Calamity Loan — available to members in areas declared under state of calamity. Borrow up to 80% of savings at 5.95% interest. 24 months to pay.

- Housing Loan — for members with at least 24 monthly contributions. Affordable home financing with interest rates from 6.5%.

- MP2 Savings — a voluntary savings program with 6-7% tax-free annual dividends, higher than any regular savings account. Lock-in period of 5 years. You can start with as little as P500.

- Total Accumulated Value (TAV) — your contributions plus dividends, returned to you when you reach 65 or become permanently disabled.

- Multi-Purpose Loan (MPL) — manghiram ng hanggang 80% ng kabuuang ipon pagkatapos ng 24 months ng contributions. Mababang interest sa 10.5% bawat taon. Bayaran sa loob ng hanggang 24 months.

- Calamity Loan — available sa mga miyembro sa mga lugar na idineklara under state of calamity. Manghiram ng hanggang 80% ng savings sa 5.95% interest. 24 months ang bayaran.

- Housing Loan — para sa mga miyembro na may hindi bababa sa 24 monthly contributions. Abot-kayang home financing na may interest rates mula 6.5%.

- MP2 Savings — voluntary savings program na may 6-7% tax-free annual dividends, mas mataas kaysa sa kahit anong regular savings account. Lock-in period ng 5 taon. Maaari kang magsimula sa P500 lang.

- Total Accumulated Value (TAV) — ang iyong contributions plus dividends, ibabalik sa iyo kapag naabot mo ang 65 o naging permanently disabled.

For the full Pag-IBIG guide, see our complete Pag-IBIG guide.

Para sa buong Pag-IBIG guide, tingnan ang aming kumpletong Pag-IBIG guide.

Where and How to Pay

Saan at Paano Magbabayad

You don't need to line up at government offices every month. Here are all the ways to pay your SSS, PhilHealth, and Pag-IBIG contributions:

Hindi mo na kailangang pumila sa government offices buwan-buwan. Narito ang lahat ng paraan para magbayad ng SSS, PhilHealth, at Pag-IBIG contributions mo:

E-Wallets (Easiest)

E-Wallets (Pinakamadali)

- GCash — Pay Bills > Government > SSS / PhilHealth / Pag-IBIG. Free or minimal fees. Available 24/7.

- Maya — Pay Bills > Government. Same convenience, same agencies. Also works with most banks.

- GCash — Pay Bills > Government > SSS / PhilHealth / Pag-IBIG. Libre o minimal na fees. Available 24/7.

- Maya — Pay Bills > Government. Parehong convenience, parehong mga ahensya. Gumagana rin sa karamihan ng mga bangko.

Over-the-Counter

Over-the-Counter

- 7-Eleven / CLiQQ kiosks — available nationwide, open late. Small convenience fee (P10-15).

- Bayad Center — found inside malls, Robinsons, and standalone locations.

- SM Bills Payment / Robinsons Business Center — pay at any SM or Robinsons mall.

- Cebuana Lhuillier / M Lhuillier / Palawan Express — pawnshop payment centers, available in most barangays.

- 7-Eleven / CLiQQ kiosks — available nationwide, bukas hanggang gabi. Maliit na convenience fee (P10-15).

- Bayad Center — matatagpuan sa loob ng mga malls, Robinsons, at standalone locations.

- SM Bills Payment / Robinsons Business Center — magbayad sa kahit anong SM o Robinsons mall.

- Cebuana Lhuillier / M Lhuillier / Palawan Express — pawnshop payment centers, available sa karamihan ng mga barangay.

Bank and Online

Bank at Online

- Bank apps — BPI, BDO, Metrobank, UnionBank, and others have government bills payment features.

- SSS / PhilHealth / Pag-IBIG branches — pay directly at any branch. Longest lines but no fees.

- Bank apps — BPI, BDO, Metrobank, UnionBank, at iba pa ay may government bills payment features.

- SSS / PhilHealth / Pag-IBIG branches — magbayad nang direkta sa kahit anong branch. Pinakamahabang pila pero walang fees.

AlkanSSSya: Save P11/Day Toward SSS

AlkanSSSya: Mag-ipon ng P11/Araw para sa SSS

The AlkanSSSya Program is an SSS + DSWD initiative designed specifically for informal workers who find monthly lump-sum payments difficult. The concept is simple: save small amounts daily (as little as P11/day), pool them with your community, and pay SSS contributions as a group.

Ang AlkanSSSya Program ay isang SSS + DSWD na inisyatiba na dinisenyo para sa mga informal workers na nahihirapan sa buwanang lump-sum payments. Simple ang konsepto: mag-ipon ng kaunti araw-araw (kahit P11/araw lang), i-pool kasama ang iyong komunidad, at magbayad ng SSS contributions bilang grupo.

How It Works

Paano Ito Gumagana

- A community group (barangay, market association, drivers' cooperative, etc.) forms an AlkanSSSya group

- Members save daily using a coin bank or collection system — as little as P11/day adds up to P330/month

- A designated collector pools the savings and remits the SSS contributions for the group quarterly

- SSS provides the group with support materials, monitoring, and enrollment assistance

- Isang community group (barangay, market association, drivers' cooperative, atbp.) ay bumubuo ng AlkanSSSya group

- Ang mga miyembro ay nag-iipon araw-araw gamit ang alkansya o collection system — kahit P11/araw lang, nagiging P330/buwan

- Isang itinalagang collector ang nag-po-pool ng ipon at nagre-remit ng SSS contributions para sa grupo quarterly

- Nagbibigay ang SSS sa grupo ng support materials, monitoring, at enrollment assistance

In 2026, the SSS expanded AlkanSSSya coverage to 4Ps beneficiaries, making it even easier for the poorest households to build toward SSS benefits. Ask your barangay captain or DSWD link about starting or joining an AlkanSSSya group in your area.

Noong 2026, pinalawak ng SSS ang AlkanSSSya coverage sa 4Ps beneficiaries, na ginagawang mas madali para sa pinakamahirap na sambahayan na mag-build toward SSS benefits. Magtanong sa iyong barangay captain o DSWD link tungkol sa pagsisimula o pag-join ng AlkanSSSya group sa inyong lugar.

Even if you can't afford the full P750/month, any progress toward your 120-month requirement counts. Partial years still build toward your pension. Don't let the perfect be the enemy of the good.

Kahit hindi mo kayang bayaran ang buong P750/buwan, anumang progreso patungo sa 120-month requirement mo ay counted. Ang partial years ay nagbi-build pa rin toward pension mo. Huwag hayaang ang paghahanap ng perpekto ay maging kalaban ng mabuti.

Government Programs That Help

Mga Programa ng Gobyerno na Tumutulong

If you're struggling to make ends meet, these government programs can supplement your income while you build your SSS/PhilHealth/Pag-IBIG contributions:

Kung nahihirapan kang magkasya ang kita, ang mga programa ng gobyerno na ito ay maaaring mag-supplement sa iyong kita habang nagbi-build ka ng SSS/PhilHealth/Pag-IBIG contributions mo:

4Ps — Pantawid Pamilyang Pilipino Program

4Ps — Pantawid Pamilyang Pilipino Program

The government's largest poverty alleviation program with a P113 billion budget in 2026. Provides conditional cash grants for health, education, and rice to qualifying households with children 0-18 or pregnant women. Beneficiaries are identified through the DSWD Listahanan, not by direct application. See our full 4Ps guide for details on how to get included.

Ang pinakamalaking poverty alleviation program ng gobyerno na may P113 bilyong budget sa 2026. Nagbibigay ng conditional cash grants para sa kalusugan, edukasyon, at bigas sa mga qualifying na sambahayan na may mga anak na 0-18 o buntis. Ang mga beneficiary ay tinutukoy sa pamamagitan ng DSWD Listahanan, hindi sa pamamagitan ng direktang pag-apply. Tingnan ang aming buong 4Ps guide para sa mga detalye kung paano maisama.

DOLE TUPAD — Emergency Employment

DOLE TUPAD — Emergency Employment

Tulong Panghanapbuhay sa Ating Disadvantaged/Displaced Workers provides 10 to 90 days of emergency employment at the prevailing minimum wage in your region. Community-based projects like clean-up drives, road maintenance, or disaster response. Apply through your barangay or the nearest DOLE field office. Priority is given to displaced workers, especially during calamities or economic downturns.

Ang Tulong Panghanapbuhay sa Ating Disadvantaged/Displaced Workers ay nagbibigay ng 10 hanggang 90 araw na emergency employment sa prevailing minimum wage sa iyong rehiyon. Mga community-based projects tulad ng clean-up drives, road maintenance, o disaster response. Mag-apply sa iyong barangay o sa pinakamalapit na DOLE field office. Prayoridad ang mga displaced workers, lalo na sa panahon ng kalamidad o economic downturns.

DOLE Kabuhayan — Livelihood Assistance

DOLE Kabuhayan — Livelihood Assistance

Provides livelihood starter kits and seed capital of up to P20,000 for individuals or up to P200,000 for groups/cooperatives. Covers tools, equipment, and raw materials for micro-enterprises. Apply at DOLE regional or field offices with a simple business plan.

Nagbibigay ng livelihood starter kits at seed capital na hanggang P20,000 para sa indibidwal o hanggang P200,000 para sa mga grupo/kooperatiba. Sinasaklaw ang mga kagamitan, equipment, at raw materials para sa micro-enterprises. Mag-apply sa DOLE regional o field offices na may simpleng business plan.

DSWD SLP — Sustainable Livelihood Program

DSWD SLP — Sustainable Livelihood Program

Provides seed capital grants for micro-enterprise development and skills training for 4Ps beneficiaries and other poor households. Includes micro-enterprise track (start your own small business) and employment facilitation track (job matching and training). Coordinate through your DSWD regional office. See our DSWD assistance guide for how to access these programs.

Nagbibigay ng seed capital grants para sa micro-enterprise development at skills training para sa 4Ps beneficiaries at iba pang mahirap na sambahayan. Kasama ang micro-enterprise track (magsimula ng sariling maliit na negosyo) at employment facilitation track (job matching at training). I-coordinate sa iyong DSWD regional office. Tingnan ang aming DSWD assistance guide kung paano ma-access ang mga programang ito.

Pro Tips

Mga Payo

- Pay quarterly if monthly is hard. PhilHealth accepts quarterly payments (P1,500 every 3 months). Easier to save up from a good week's earnings than to set aside money every month.

- Use GCash or Maya to skip the lines. No need to travel to a branch. Pay from your phone at home, at the palengke, or wherever you are. Saves you a half-day of lost income from queueing.

- Check your SSS contributions on My.SSS regularly. Log in at my.sss.gov.ph to verify all payments are posted. Payments without a PRN can go missing — catch errors early.

- If you're close to 120 months on SSS, don't stop. Even if money is tight, pushing through to 120 months guarantees you a lifetime monthly pension. Every month counts.

- Kasambahay employers are required by law to pay your SSS, PhilHealth, and Pag-IBIG. Under the Kasambahay Law (RA 10361), your employer must register you and share the cost. If they're not paying, show them the law. See our Kasambahay Law guide.

- PhilHealth covers your dependents too. Your spouse and children under 21 are automatically covered under your PhilHealth membership. One ₱500/month payment protects your whole family.

- Magbayad quarterly kung mahirap ang monthly. Tumatanggap ang PhilHealth ng quarterly payments (P1,500 kada 3 buwan). Mas madaling magtabi mula sa magandang linggo ng kita kaysa mag-set aside ng pera buwan-buwan.

- Gumamit ng GCash o Maya para i-skip ang mga pila. Hindi na kailangang bumiyahe sa branch. Magbayad mula sa phone mo sa bahay, sa palengke, o saan ka man. Nakakatipid ng kalahating araw na nawalan ng kita dahil sa pagpila.

- I-check ang SSS contributions mo sa My.SSS regularly. Mag-log in sa my.sss.gov.ph para i-verify na lahat ng bayad ay naka-post. Ang mga bayad na walang PRN ay maaaring mawala — mahuli ang mga error nang maaga.

- Kung malapit ka na sa 120 months sa SSS, huwag tumigil. Kahit mahirap ang pera, ang pag-push through sa 120 months ay nag-ga-guarantee ng lifetime monthly pension. Bawat buwan ay counted.

- Ang mga employer ng kasambahay ay required by law na bayaran ang SSS, PhilHealth, at Pag-IBIG mo. Sa ilalim ng Kasambahay Law (RA 10361), dapat ka nilang i-register at hatian ang gastos. Kung hindi sila nagbabayad, ipakita mo sa kanila ang batas. Tingnan ang aming gabay sa Kasambahay Law.

- Sinasaklaw ng PhilHealth ang mga dependents mo rin. Ang asawa mo at mga anak na wala pang 21 ay awtomatikong covered sa ilalim ng PhilHealth membership mo. Isang ₱500/buwan na bayad ay nagpoprotekta sa buong pamilya mo.

Frequently Asked Questions

Mga Madalas Itanong

I only earn P300-500 a day. Is P1,450/month for all three really worth it?

P300-500 lang ang kinikita ko sa isang araw. Sulit ba talaga ang P1,450/buwan para sa tatlo?

You don't have to pay all three at once. Start with PhilHealth only (₱500/month) — that alone gives you hospital coverage that can save P50,000-P600,000 in a single emergency. Add SSS and Pag-IBIG when you're able. See the priority ladder above.

Hindi mo kailangang bayaran ang tatlo nang sabay. Magsimula sa PhilHealth lang (₱500/buwan) — iyon lang ay nagbibigay na ng hospital coverage na maaaring makatipid ng P50,000-P600,000 sa isang emergency. Idagdag ang SSS at Pag-IBIG kapag kaya mo na. Tingnan ang priority ladder sa itaas.

What happens if I miss payments for a few months?

Ano ang mangyayari kung hindi ako makabayad ng ilang buwan?

SSS: Your membership doesn't expire, but benefit eligibility depends on recent contributions. You can resume anytime without penalty. PhilHealth: You need at least 9 months of contributions within the past year for full inpatient benefits, but Konsulta (outpatient) is available regardless. Pag-IBIG: Contributions stay in your account; you can resume anytime.

SSS: Hindi mag-eexpire ang membership mo, pero ang eligibility sa benefits ay depende sa recent contributions. Maaari kang mag-resume anumang oras nang walang penalty. PhilHealth: Kailangan mo ng hindi bababa sa 9 months ng contributions sa nakaraang taon para sa full inpatient benefits, pero ang Konsulta (outpatient) ay available kahit ano pa. Pag-IBIG: Nananatili ang contributions sa account mo; maaari kang mag-resume anumang oras.

Do I need an employer to join SSS, PhilHealth, or Pag-IBIG?

Kailangan ko ba ng employer para sumali sa SSS, PhilHealth, o Pag-IBIG?

No. All three agencies accept voluntary or self-employed members. You register yourself, choose your contribution amount (at or above the minimum), and pay directly. No employer needed.

Hindi. Ang tatlong ahensya ay tumatanggap ng voluntary o self-employed members. Ikaw mismo ang magre-register, pipili ng contribution amount mo (sa o higit sa minimum), at direktang magbabayad. Walang employer na kailangan.

What benefits do I get for just ₱750/month in SSS?

Ano ang makukuha kong benepisyo sa ₱750/buwan sa SSS?

Sickness benefit (90% of daily credit, up to 120 days), maternity (100% for 105 days), disability pension, funeral benefit (₱20,000–₱60,000), salary loan after 36 months, and a guaranteed retirement pension after 120 months. See the full breakdown in the SSS section.

Sickness benefit (90% ng daily credit, hanggang 120 araw), maternity (100% sa loob ng 105 araw), disability pension, funeral benefit (₱20,000–₱60,000), salary loan pagkatapos ng 36 months, at garantisadong retirement pension pagkatapos ng 120 months. Tingnan ang buong breakdown sa SSS section.

Can I pause and resume contributions later?

Maaari ba akong tumigil at mag-resume ng contributions mamaya?

Yes. All three agencies allow you to stop and restart without losing your previous contributions. Your accumulated months still count toward eligibility thresholds (e.g., SSS 120-month pension requirement). Just resume paying when you can.

Oo. Ang tatlong ahensya ay nagpapahintulot na tumigil at mag-restart nang hindi mawawala ang mga nakaraang contributions mo. Ang naipon mong months ay counted pa rin sa eligibility thresholds (hal., SSS 120-month pension requirement). Mag-resume lang ng pagbabayad kapag kaya mo na.

I'm a kasambahay. Should I be paying for these myself?

Kasambahay ako. Dapat ba akong nagbabayad nito nang mag-isa?

No. Under the Kasambahay Law (RA 10361), your employer is required to register you with SSS, PhilHealth, and Pag-IBIG and share the cost of contributions. For kasambahay earning P5,000 or less, the employer pays the full premium. See our Kasambahay Law guide for your full rights.

Hindi. Sa ilalim ng Kasambahay Law (RA 10361), kinakailangan ang employer mo na i-register ka sa SSS, PhilHealth, at Pag-IBIG at hatian ang gastos ng contributions. Para sa kasambahay na kumikita ng P5,000 o mas mababa, ang employer ang nagbabayad ng buong premium. Tingnan ang aming gabay sa Kasambahay Law para sa buong karapatan mo.